As we approach the 2024 Presidential election and the contenders present themselves to the voters, I assess the candidates, just like everyone else. I have previously stated one essential quality I am looking for in a President: fiscal responsibility. But, of course, there are other important attributes as well. Here is my first attempt to describe these essential qualities in a coherent way. Three of the most important:

- An optimistic vision for the future of America. We are the strongest and freest country in the world for many reasons. We aspire to equal opportunity for everyone and work hard to achieve this ambitious goal. When we fall short, for example, with poor educational outcomes, educational choice springs up in the form of charter schools and/or private school vouchers. We put a strong emphasis on economic growth and opportunity. It is no accident that we are a highly innovative society because our economic system encourages growth and development.

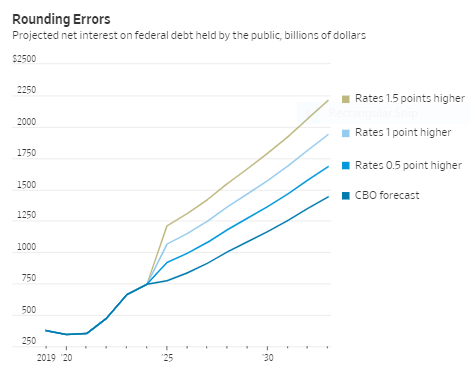

- Fiscal responsibility. One of the major themes on this blog is the urgent need for fiscal responsibility from national leaders. Our huge and rapidly growing national debt is unsustainable. The $5 trillion pandemic spending blowout tripped off inflation starting in early 2021, which has forced the Federal Reserve to raise short-term interest rates to 5.25% so far and perhaps higher. This enormously increases interest payments on the debt that, in turn, makes our deficits and accumulated debt much worse. The debt problem cannot be fully addressed without major reforms in entitlement spending.

- A hawkish view of national security. Although we are the strongest nation in the world, we have two major rivals for predominance, China and Russia. It is critical that we continue to help Ukraine defend itself from the Russian invasion. It is not only the morally right thing to do but also in our own best interest to defend freedom and democracy around the world. Our help for Ukraine, for example, will likely deter China from trying to invade Taiwan.

- Republican presidential candidates. Based on her performance in the first presidential debate, see here and here, Nikki Haley is the only candidate in either party so far who meets all three of the above essential requirements to be President. She has an inspiring personal story, she understands the seriousness of our debt problem, and she supports our defense of Ukraine.

Conclusion. Being optimistic about the future of America, understanding the seriousness of our debt problem, and being committed to the strong defense of freedom and democracy around the world, are three very important qualities needed by our next President. So far, Nikki Haley is the only candidate in either party who has demonstrated these essential qualities. Much further discussion on this issue will follow as the campaign proceeds!

For my Email Newsletter

Follow me on Facebook

Follow me on Twitter