On this blog, I discuss important national issues, often concerning fiscal and economic matters. Most recently, I have been discussing overall U.S. strength, economic and military, and U.S. indispensability as the leader of the free world.

But there is a significant threat to continued U.S. world hegemony, and this is what I will address today. First of all, I list several factors which are not serious problems at the present time. Consider:

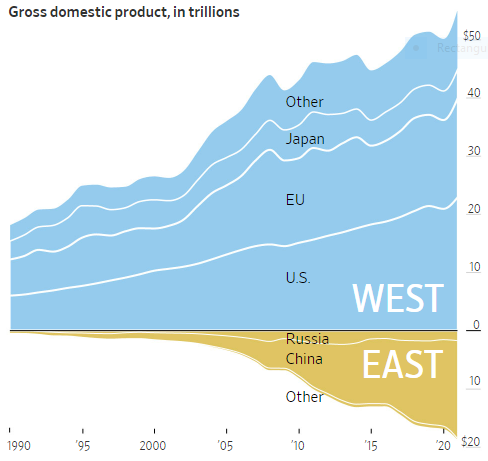

- The U.S. and its allies totally dominate the world economy. The U.S. economy, at $30 trillion, is half again as large as the Chinese economy, the second largest in the world, at $19 trillion. Furthermore, the U.S. and its allies swamp out the economies of China and its autocratic allies (see chart below).

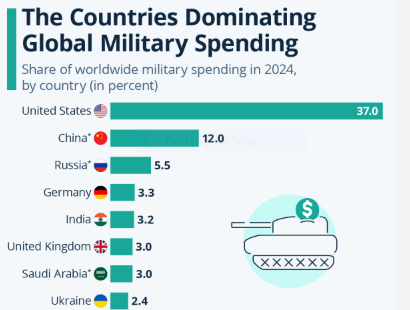

- Militarily, again the U.S. and its major allies greatly outspend China and its major allies (see chart below).

- With respect to Artificial Intelligence, the emerging engine of economic growth, again, the U.S. totally dominates private investment in A.I. (see chart below). We also currently have a large lead in the production of computer chips. Furthermore, A.I. is likely to eventually subvert communism because of its inherently open features.

But the U.S. does have a very serious problem which must be addressed in the near future: our very large and rapidly growing national debt. U.S. debt now stands at $39 trillion and is growing at the unsustainable rate of $2 trillion per year. Tax revenue amounts to about $5 trillion per year but the U.S. is spending $7 trillion per year. The biggest single measure that must be adopted to greatly shrink our annual deficit spending is entitlement reform: especially for Social Security and Medicare. They must be made much more self-supporting than they are at the present time

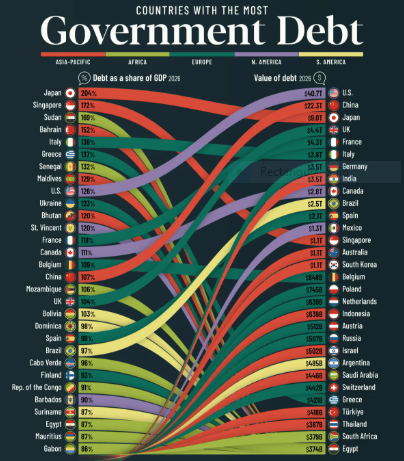

A somewhat mitigating factor regarding the debt issue, is the fact that many other countries also have debt problems (see chart below). In fact, the U.S. is 9th overall worldwide in terms of national debt, as a percentage of GDP, at 126%. China ranks 16th highest with its debt at 107% of GDP.

How is the debt issue likely to play out? At some point, our debt may become unattractive to investors, or at least cause interest rates to rise, which is already happening to a certain extent. But whose debt will investors turn to instead? This is not clear with so much debt outstanding around the world.

Conclusion. The U.S. is the dominant world hegemon at the present time and this is very important in preserving democracy and world peace. But massive growth of U.S. debt threatens this rosy scenario. The U.S. needs to come to its senses, debt-wise, the sooner, the better, before its worldwide dominance is seriously threatened by a less attractive and perhaps autocratic, as opposed to democratic, rival.

Follow me on Twitter

Follow me on Facebook