The Congressional Budget Office has just released its analysis of the GOP Healthcare Reform Bill, the American Health Care Act, designed to replace the Affordable Care Act. The Committee for a Responsible Federal Budget has summarized its main features as follows:

- The AHCA would reduce federal deficits by $337 billion over the next ten years.

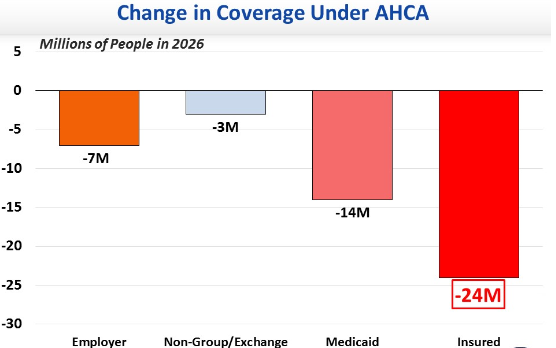

- CBO estimates that there would be 24 million fewer Americans with health insurance under the AHCA as compared with the ACA by 2026, with 14 million fewer Medicaid beneficiaries (see the above chart). The decrease in individuals with employer coverage would result from dropping the employer mandate. The decrease in individual coverages would result from smaller subsidies under the AHCA.

I have previously summarized the AHCA pointing out its strengths and weaknesses:

- Strengths: discards mandates, fewer regulations, turns Medicaid into block grant program to states.

- Weakness: huge discrepancy between lavish tax treatment of employer-paid care (no upper limit on tax exemption) and much stingier tax credits for individuals

The U.S. now spends 18% of GDP on healthcare, both public and private, almost twice as much as any other developed country. Such high costs are a big drain on government revenue as well as a drag on economic growth. The AHCA should take a much bigger step towards controlling the cost of healthcare. Block granting Medicaid to the states, and giving the states more flexibility in implementation, definitely helps, but it is not enough.

But basic fairness as well as fiscal responsibility requires a major cutback in the tax exemption for employer provided care. This is essentially a subsidy to employees. It should have no greater value than the refundable tax credit provided to individuals who purchase health insurance on their own.

Conclusion. A free market healthcare system allows more individual choice and delivers more medical innovation. But our current system is too expensive to be sustainable for much longer. Either the GOP fixes this problem or a single-payer system will be the inevitable result.

Follow me on Twitter

Follow me on Facebook

As a starting point, ACHA 2017 (aka TrumpCare) begins with an attempt to improve the financial efficiency of our nation’s healthcare. However, it will need an effort to decrease the number of citizens who lose coverage as it stands for now. And, more importantly, the need to solve the substantial variability, community by community, in the uniform quality of Primary Healthcare is left untouched. Meanwhile, our nation’s maternal mortality ratio continues to worsen by a lot. We now rank 45th worst among the world’s 46 developed nations. And the number of our nation’s medicare eligible citizens continues to increase on the path of doubling between 2000 and 2030. Just for perspective, a random group of 100 citizens over age 65 will cost about 10 times as much for their annual healthcare as a random group of 100 citizens between age 25 and age 64 for their healthcare.

.

Furthermore, we have absolutely NO PLAN to *) encourage each community, nation wide, to systematically identify and then use collective action to ameliorate the essential adversities that affect the HEALTH of its citizens and *) assure that the resiliency of the community’s high-risk disaster plan is maintained (as a basis for managing its unpredictable disasters such as an influenza pandemic). It seems odd that the major players within healthcare finance do not seem overtly very vocal: Primary Physicians (Family Medicine, Pediatrics, Internal Medicine), PHARMA, Academy of Medicine, American Association of Medical Colleges). Ben Franklin said it best, “If we don’t hang together, we will all hang separately.” (before signing the new Constitution)

.

I cite the following: “The economic and political performance of societies, from villages to international communities, depends critically on how the members of a community solve the problems of collective action. Contemporary theorists of social capital, almost without exception, open their discourse on social capital by placing the problem of collective action at the center of our economic and political problems.” I took this quotation from the ‘Introduction’ to the book FOUNDATIONS OF SOCIAL CAPITAL published in 2003 and edited by Elinor Ostrom and T.K. Ahn.

It is a good idea to try to understand the variability, from one community to another, in healthcare quality but this is really beyond the scope of the AHCA. Likewise the AHCA does not address the problem of Medicare expansion which we know will be huge.

What the AHCA does do is to address the unsustainability of Medicaid as currently operated. It is a disaster for both state budgets and the federal budget. More on this in my next post.

Jack,

If you read the CBO assessment it’s absolutely clear that compared to today, nongroup coverage will expand per CBOs projections. The current non group market is around the 17 million, while the CBOs projection for 2026 is that the non group market will be 22 million.

I’m not sure there’s a huge difference between the value of the tax exclusion and the tax credit. For many healthy, younger workers, the value of the credit will likely exceed the value of the tax exclusion.

It will expand under the AHCA that is*

The problem is that there is no limit on the value of the employer tax exclusion and this is the main driver of the cost of American healthcare. Under the AHCA the tax credit is the same for all, rich and poor alike, whereas it ought to be means adjusted.

Agree that there should be a limit on tax exclusion, however the value of the tax credit is higher then the value of the tax exclusion in most cases.

I don’t think I agree with you that the credit should be means adjusted. That’s the central flaw of the PPACA, and re-enacting that central flaw isn’t helpful. It’s easier and more efficient to create progressivist through the tax code then through these credits.

I don’t think you’re right about this. The unlimited tax exclusion can and does exceed $20,000 for a family of four. The AHCA tax credits are much smaller than this. Really what we should have for both efficiency and fairness is a universal (and equal) tax credit for all, equal to the cost of catastrophic health care. And then also perhaps tax preferred health savings accounts to pay for routine healthcare expenses. I realize that this is a long reach from where we are at the present time.

Jack,

A tax exclusion of $20,000 at a marginal tax rate of 25% Income+7.65% Payroll is worth around $6500 compared to an average AHCA tax credit of $8-9000 for that same family of four. I don’t think that family of four is better off taking the tax exclusion vs. a tax credit and getting that $20,000 in cash wages. Now it’d be a different story if that family can’t trade the healthcare exclusion in for cash wages of course…

This is getting too complicated! Ideally everyone would get the same (refundable) tax credit equal to the cost of catastrophic care. Then there could be means-adjusted subsidies to se up health savings accounts to cover routine healthcare expenses. The goal is universal coverage with individual responsibility built in.