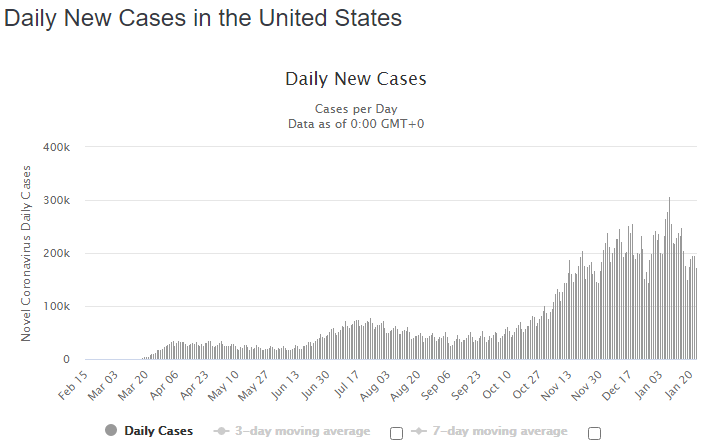

As President Joe Biden takes office, the coronavirus daily infection rate is beginning to drop significantly and vaccines are rolling out. Most Americans will soon be back to work and schools will reopen full time.

As I pointed out in my last post, fundamental inflationary forces, caused by world-wide demographic changes, are starting to reappear in the world economy. This will have a serious negative consequence for our national debt by dramatically increasing interest rates and, therefore, interest payments on the debt.

Furthermore, even short term inflationary forces are rearing their heads:

- Five-year inflationary expectations are growing rapidly.

- S. fiscal stimulus (including Biden’s new $1.9 trillion proposals), is massive by world standards.

In evaluating the need for more stimulus, it is important to take into account the underlying strength of the economy:

- Median U.S. household income has grown dramatically in recent years and was $68,703 at the end of 2019, right before the pandemic hit.

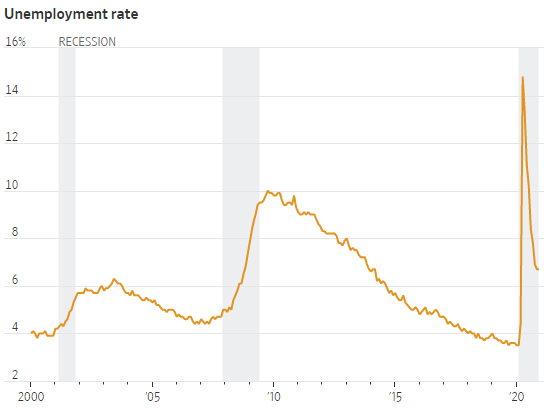

- The unemployment rate, a very low 3.5% when the pandemic hit, has already dropped back down to 6.7% from a pandemic high of over 14%.

- The federal debt held by the public, now $21.3 trillion, is a very high (and rapidly growing) 99.4% of GDP.

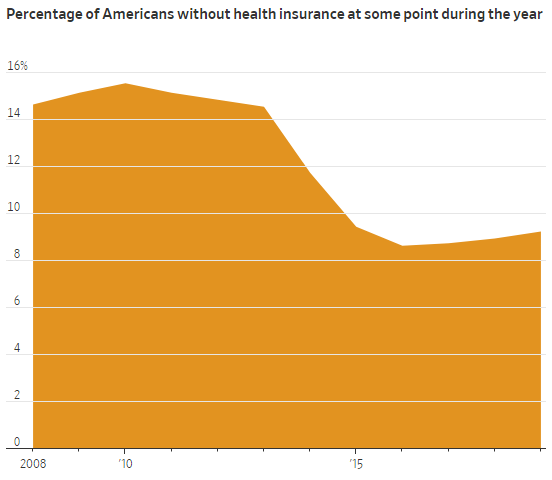

- Only a relatively low 9.2% of U.S. citizens are without health insurance, the lowest number in many years.

The above overall data show the good shape of the American economy, as we are pulling out of the pandemic. All of these factors indicate a need for restraint in providing additional fiscal stimulus.

Conclusion. The combination of the underlying good health of the U.S. economy plus the building up of inflationary forces worldwide, suggest that any additional fiscal stimulus for the U.S. economy at the present time should be quite limited.

Sign-up for my Email Newsletter

Follow me on Facebook

Follow me on Twitter

https://mail.yahoo.com/n/list/folders=1&listFilter=ALL_INBOX/messages/AABvxqUw5fp7DHMs5MqX9FU1lRz?.src=ym&reason=myc

Thanks for pointing this out to me. This post is several years old. I am aware that the current US median household income is about $80,000.