“Our responsibility to deliver price stability is unconditional. We are committed to doing that job” Jerome Powell. Jackson Hole. August 26, 2022

Last week I wrote that we should be optimistic about the future of our country. I discussed several major trends that are going in the right direction. But, of course, we do have one big problem right now which may get worse before it gets better. I’m talking about price inflation.

What Mr. Powell basically said by implication at Jackson Hole is that “inflation must be beat, and it won’t be pretty.” The problem is made more difficult because the Fed is fighting several headwinds at the same time. Consider:

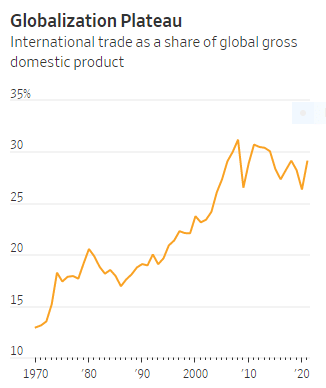

- Globalization. In the 1990s multinational companies constructed global supply chains focused on driving down costs by finding the cheapest place and workers to produce products. After the pandemic and the Ukraine war disrupted supply chains, many business leaders adopted new processes to increase reliability even if they cost more, such as by moving production closer to home or buying from multiple suppliers. In other words, globalization is now on hold (see chart). This means higher prices for many items.

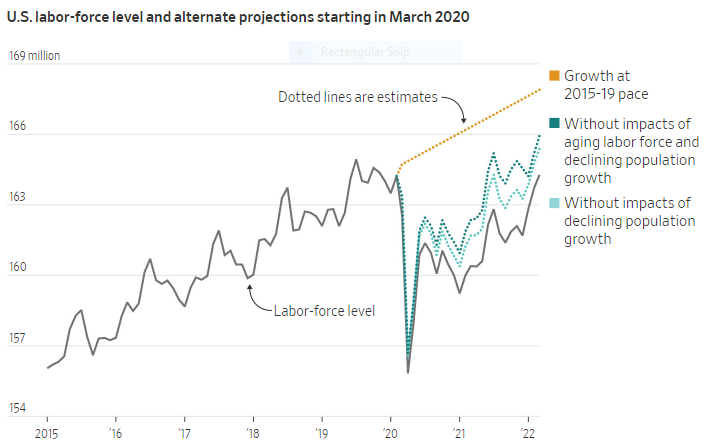

- Labor markets. The U.S. labor force has roughly 2.5 million fewer workers than since the pandemic began compared with what it would have been if the pre-pandemic trend in workforce participation had continued, and after accounting for the aging of the population (see chart). This means that labor costs are rising faster than usual.

- Energy, commodity prices. For various reasons, energy and commodity firms haven’t heavily invested in new production over the past decade, creating risks of more persistent shortages when global demand is growing. This, of course, also raises prices.

- Fiscal policy. As I have previously discussed, President Biden’s spending policies, including the so-called Inflation Reduction Act, in the past year alone, have increased deficit spending in the short term. And this doesn’t take into account the inflationary effects of the student debt forgiveness plan, which will cost roughly $500 billion over a ten-year period, as well as driving up the costs of higher education and loans going forward.

Conclusion. The $5 trillion Covid stimulus spending tripped off the latest inflationary spiral which has now reached 8.5% as of July 2022. So far, the Fed has raised short-term interest rates 2.5 percentage points and will have to raise them much higher in order to bring inflation back down to the desired 2% level. Each 1% sustained increase will increase interest payments on our national debt by over $200 billion per year which will make our annual deficits, currently running at about $1 trillion per year, that much worse. This is a huge problem that must be urgently addressed. It can be solved, of course, but it will take a great deal of fiscal responsibility (i.e. cost cutting) to get the job done. Are we up to this major challenge?

for my Email Newsletter

Follow me on Facebook

Follow me on Twitter