I began writing this blog in November 2012, right after the 2012 national election when Barack Obama was reelected to a second term as President. Under Obama our biggest problems were: 1) slow economic growth (2% annually since June 2009) and 2) massive and rapidly increasing debt, now 77% of GDP.

After the surprise victory of Donald Trump last fall, my perspective has changed a little bit. Slow growth is still a huge problem. My last several posts have, in fact, focused on the despair of many blue-collar workers who have been harmed by our stagnant economy in recent years.

Mr. Trump was strongly supported by blue-collar workers last fall and clearly wants to help them out. Faster economic growth will accomplish this and President Trump is working with the Republican Congress to get this done through tax and regulatory reform. I’m optimistic that progress will be made along these lines.

But our debt problem has not really been addressed so far by the Trump Administration. James Capretta from the American Enterprise Institute gives a good summary of where we are:

- Entitlement Spending is the Problem. In 1972 the federal government spent a combined 4.2% of GDP on Social Security, Medicare and Medicaid. In 2016 spending on these programs was 10.4% of GDP. The Congressional Budget Office predicts that this figure will jump to 13.5% of GDP in 2030 and 15.6% of GDP in 2047 unless current policy is changed.

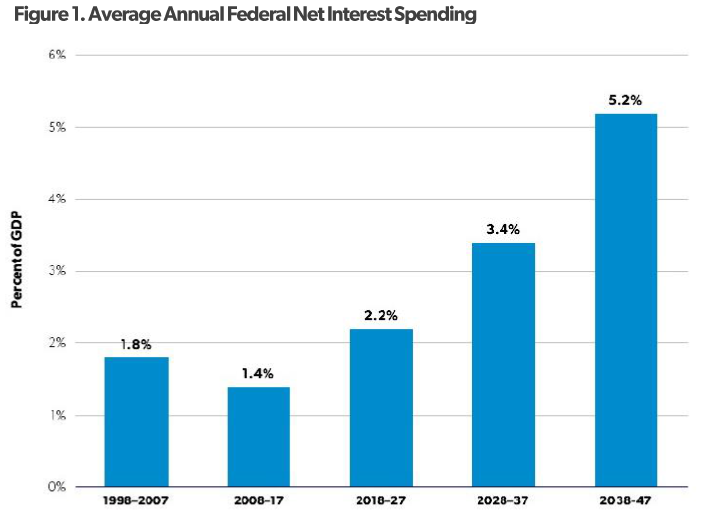

- The Fiscal Consequences of Interest Rate Normalcy. In 2008 when federal debt was at 39% of GDP, federal spending on net interest payments was 1.7% of GDP. For 2017 net interest payments will be just 1.3% of GDP even though the federal has doubled since 2008. This is due to the abnormally low interest rate of 2.3% at the present time. CBO projects that the interest rate on 10-year Treasury notes will rise to 3% in 2019-2020 and 3.6% for the period 2021-2027.

Conclusion. Right now our huge and rapidly increasing debt is almost “free money” because interest rates are so low. This can’t and won’t last. As interest rates inevitably climb to more normal levels, interest payments on the debt will rise precipitously. This will cause much pain by further squeezing spending on many popular programs. The only sane way to mitigate this highly unpleasant prospect is to shrink deficit spending down to zero as quickly as possible.

A surplus is the only good answer, ultimately.

Surpluses would be nice but are a pretty far reach. Just shrinking the annual deficits down closer and closer to zero would be a huge achievement and would make the debt also shrink as a percentage of GDP.