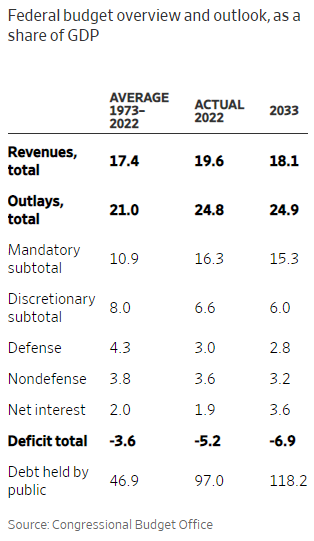

The U.S. is now in a rough patch with out-of-control spending leading to growing annual deficits, massive debt, and stubbornly high inflation. Furthermore, President Biden is virtually clueless on basic economic and fiscal policy, while the leading GOP presidential candidate for 2024, former president Donald Trump, is under one criminal indictment with more expected.

Although it is clear in a general sense what is needed to get back on track, how do we get started in the right direction?

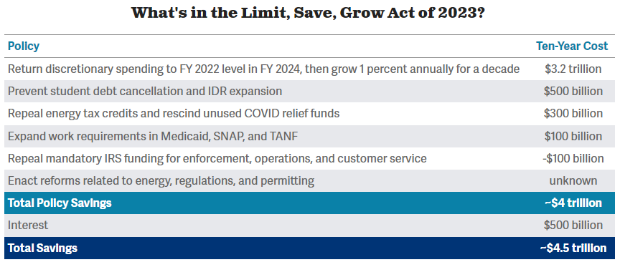

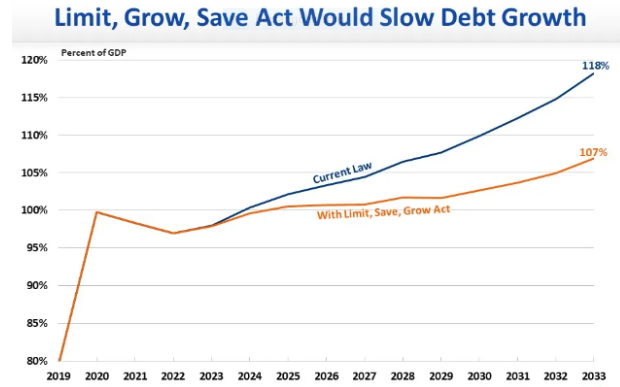

The budget bill introduced by the House Republicans, the Limit, Save, Grow Act, is an excellent way to start. It would produce savings of $4.5 trillion over ten years and improve our fiscal trajectory going forward (see charts below). The main features are:

- Return domestic spending to the level of FY 2022 and then limit growth to 1% per year for the next ten years.

- Establish a 20-hour-per-week work requirement for all able-bodied adults, between ages 18 and 59, without dependents, who receive food stamps or Medicaid. There are an estimated 40 million Americans on food stamps and 55 million on Medicaid, roughly 10% of whom would now be required to work for their welfare benefits.

- Returning all unspent Covid funds to the Treasury since the pandemic emergency is over. Additionally, stopping the forgiveness of college loan debt for students from wealthy families will save hundreds of billions of dollars.

- Raising the debt limit by $1.5 trillion or until March 31, 2024, whichever comes first. This reflects the approximately $300 billion saving under the House plan for 2024 compared to what is in President Biden’s proposed 2024 budget. The 2024 Biden budget proposal produces a deficit of $1.8 trillion next year compared to $1.5 trillion under the House plan.

- Default on the debt should not be a big concern. Enough tax revenue continuously flows into the Treasury to pay interest on the debt and also pay priorities like Social Security. Other parts of the government might have to operate briefly at reduced capacity, but this has happened before.

Conclusion. It is imperative to get federal spending under much better control to avoid a new and much worse financial crisis in the near future. The House Republican plan represents an excellent place to begin budget and debt ceiling negotiations between the House, the Senate, and the Biden Administration.

For my Email Newsletter

Follow me on Facebook

Follow me on Twitter