Last week I discussed the rough patch that our country is now in with still 6% inflation, out-of-control national debt, and fraught presidential politics. But it is possible to turn things around; this has been done so far in American history. Consider:

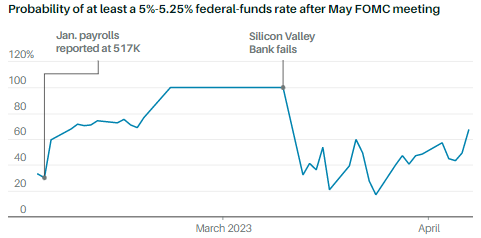

- Where we are right now. Nonfarm payrolls increased by 236,000 in March and the unemployment rate dropped from 3.6% to 3.5%. There are still almost 10,000,000 job vacancies nationally. Such a tight jobs market means that the March CPI (inflation) index is likely to be only slightly lower than February’s 6%. Therefore the Fed will likely raise rates again when it meets in early May. In other words, bringing inflation down to the desired 2% level will take longer than anticipated. (Added on April 13: since the latest inflation number,5%, is lower than I expected, I now expect that the Fed is less likely to raise rates in May. This means that inflation may linger longer).

- How do we get back to sound money and long-term prosperity? Paul Singer, the founder of Elliot Management and one of the world’s most successful hedge-fund proprietors, has predicted all of the financial crises in the last 15 years. He warned about the dangers of subprime mortgages, the excesses of the Dodd-Frank Act of 2010, and the expansive monetary policy ever since.

He is afraid that short-term declines in inflation will deceive policymakers and that they’ll quickly go back to their easy money playbook. If so, inflation will likely come roaring back, and interest rates will have to go higher for longer.

He worries that the current market trouble is only the beginning. Likely is an extended time period of jagged moves as people come to grips with the excesses in the financial system.

His optimistic scenario going forward “would entail pro-growth reforms across the board, including tax reductions, entitlement reforms, regulatory streamlining, encouraging energy development including hydrocarbons … cutting federal spending, and selling the asset holdings on central bank balance sheets.”

In other words, let us assume that Jerome Powel’s Federal Reserve can get inflation subdued soon as Paul Volcker’s did in the 1970s and 1980s. Then we will still need a president like Ronald Reagan to implement the pro-growth reforms referred to by Mr. Singer above. This is what happened in the 1980s and, with some luck, it will happen again.

Conclusion. We are in a rough patch, a fiscal, economic, and political mess. Mr. Singer is right on track for how to turn things around. If we are fortunate, American exceptionalism will assert itself and lead us back to the promised land of sound money and long-term prosperity.

For my Email Newsletter

Follow me on Facebook

Follow me on Twitter