The U.S. is in a rough patch at the present time. The long-term steps needed to restore sound money and prosperity are clear. But how do we get started?

- First, reduce inflation. Yes, inflation dropped to 5% annually in March 2023 from 6% in February. That is progress but the Federal Reserve’s remaining job will be difficult. If it continues raising short-term interest rates, it risks causing more bank failures. If it stops raising interest rates, inflation will subside much more slowly.

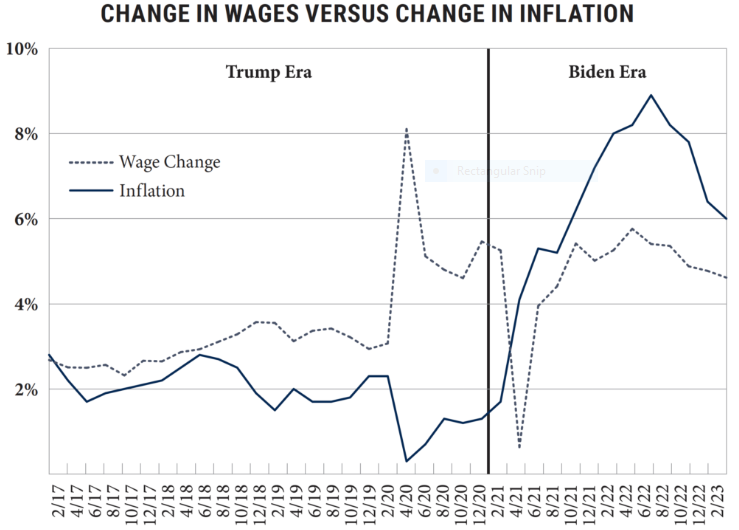

- The analyst Andrew Puzder has a good discussion of what it will take to get back to strong economic growth. Most basically, coming out of the pandemic, two things were clear. First, we knew that people had accumulated a lot of money. The federal government handed out over $5 trillion during the pandemic and people had little opportunity to spend. The second thing we knew was that fewer people were working. These two factors combined to produce excess demand and less supply than normal. In fact, the $1.9 trillion American Rescue Plan of March 2021 tripped off the ensuing inflation (see chart below).

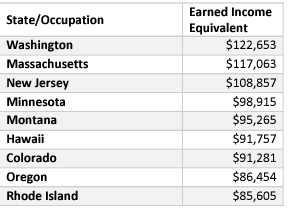

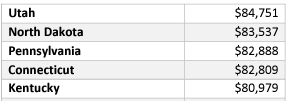

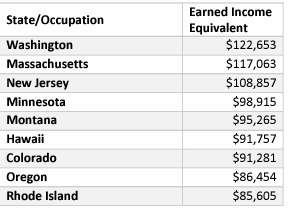

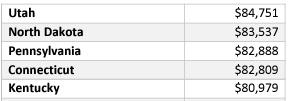

- Believe it or not, we are still paying too many Americans not to work. A study from December 2022 shows that in 24 states unemployment benefits and ACA subsidies for a family of four with both parents not working are still the annualized equivalent of at least the national median household income. Moreover, in 14 states (shown below), unemployment benefits and ACA subsidies are equivalent to a head of household earning $80,000 or more in salary, plus health insurance benefits.

Conclusion. The Federal Reserve has more work to do to bring down inflation to the desired 2% level. And the recent banking crisis is making its job harder. But the current labor shortage, which contributes to inflation by reducing supply, is unnecessarily worsened by paying too many people not to return to work.

For my Email Newsletter

Follow me on Facebook