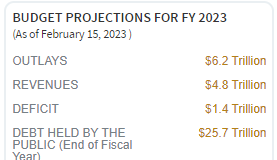

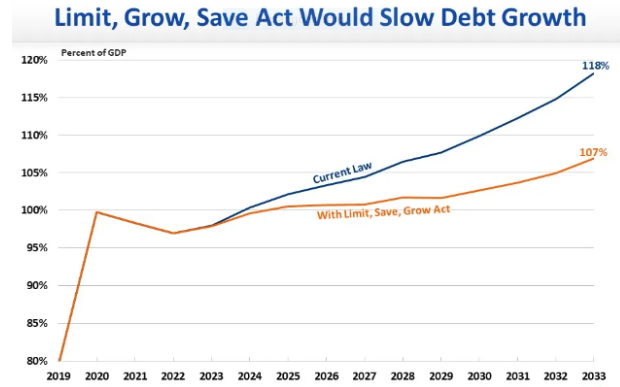

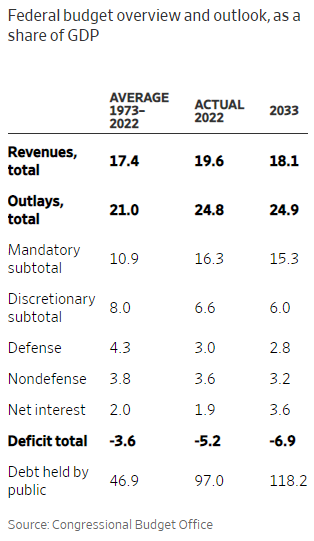

Congress has now passed, and President Biden has signed, the Fiscal Responsibility Act of 2023. It suspends the debt limit until January 2025, after the next presidential election, as well as setting an overall budget for FY 2024, beginning on October 1, 2023. According to the Congressional Budget Office (CBO), it will reduce deficit spending by $1.5 trillion over the next ten years, which is quite modest, given our very large and rapidly growing national debt of $31.4 trillion.

It is generally well understood that the entitlement programs of Social Security and Medicare are the biggest drivers of our exploding national debt. Social Security needs some relatively modest tweaks (raising the eligibility age and/or income caps). But Medicare’s future solvency is a much larger problem, which will have to be addressed soon.

It is generally well understood that the entitlement programs of Social Security and Medicare are the biggest drivers of our exploding national debt. Social Security needs some relatively modest tweaks (raising the eligibility age and/or income caps). But Medicare’s future solvency is a much larger problem, which will have to be addressed soon.

Nevertheless, the just-enacted Fiscal Responsibility Act has several excellent features:

- It reduces non-defense discretionary spending from the 2023 level of $744 billion to $704 billion for 2024, although not quite to the 2022 level of $689 billion, see here and here.

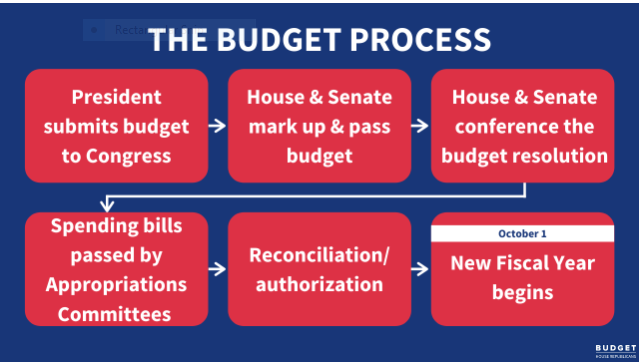

- If the House and Senate fail to enact the required 12 appropriations bills for FY 2024 by the end of this calendar year, all discretionary accounts are subject to a 1% cut. In other words, a strong incentive is created for returning to “regular order” where spending amounts are debated and voted on by the various appropriations committees in both the House and Senate, rather than Congress passing an omnibus spending bill at the last minute.

- The important principle of work requirements for welfare programs is reinforced even though only small improvements are included in the new legislation.

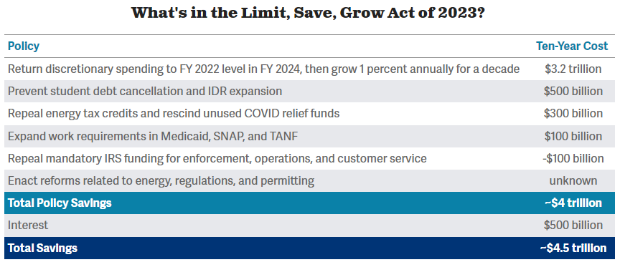

- The fulcrum of the nation’s political mood appears to be moving to the right, on such major issues as spending, crime, the border, and parental rights. The Fiscal Responsibility Act, resulting from negotiations between President Biden and House Speaker McCarthy over the House Limit, Save, Grow Bill, establishes the Republican House as the prime mover of political change in the current highly polarized national environment.

Conclusion. The new Fiscal Responsibility Act, passed by Congress and signed by President Biden, achieves only modest deficit reduction over the next ten years, but nevertheless is consistent with the somewhat conservative political mood of the American people and therefore could well lead to other valuable changes and improvements in national policy in the near future.

For my Email Newsletter

Follow me on Facebook

Follow me on Twitter