As many commentators, including myself, have pointed out, we need faster economic growth in order to create more and better paying jobs and also to bring in more tax revenue to shrink our huge budget deficits.

The rate of economic growth equals the growth of labor productivity plus the growth of employment. The problem is that both productivity growth and the labor force participation rate have dropped steeply in recent years.

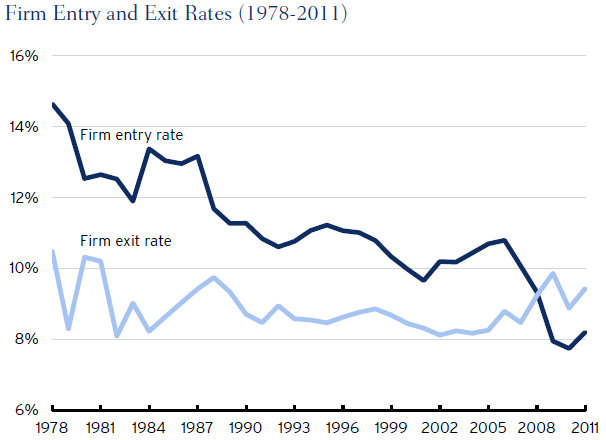

As I have pointed out in previous posts, the U.S. economy has become less entrepreneurial in recent years in the sense that there are now more firms going out of business than new firms going into business.

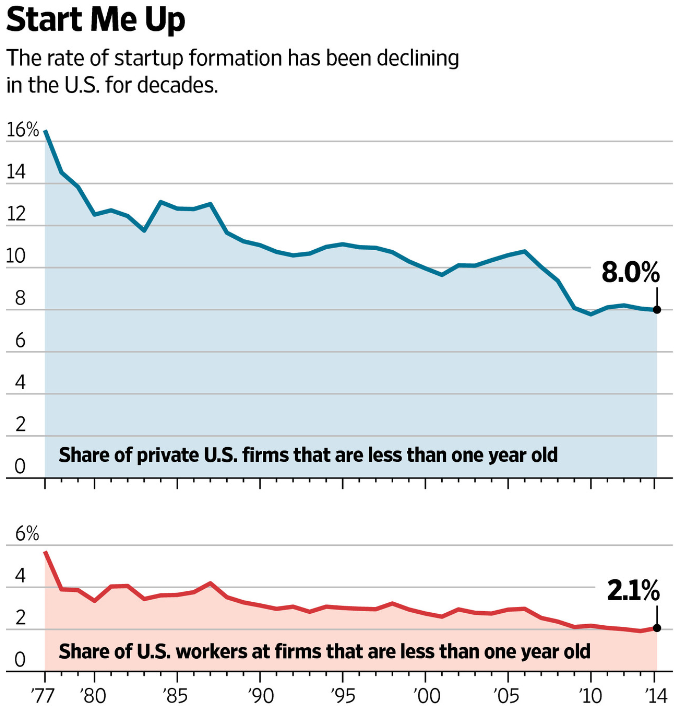

An article in yesterday’s Wall Street Journal has another way of looking at this. The rate of startup formation has been declining in the U.S. for decades (as shown just below). It is obvious that figuring out how to boost entrepreneurship would do a lot to spur economic growth.

This can be accomplished with:

- General growth measures. Tax reform (lower marginal rates paid for by shrinking deductions), regulatory reform and simplification, maximum free trade to open markets, immigration reform to bring in more skilled workers, entitlement reforms to prevent a debt explosion.

- Business tax incentives. Immediate write-off (i.e. expensing) of business investment. This encourages more investment by eliminating the need for depreciation over an arbitrary number of years. It is paid for by eliminating the deduction for interest expense to finance such investment.

Conclusion. Lots of voices are saying that technological innovation is slowing down and that only fiscal stimulus by the government can speed up growth. Such pessimistic views will predominate unless the private sector is given the tools it needs to achieve growth in the most productive way.

Follow me on Twitter

Follow me on Facebook