The Atlantic monthly magazine is celebrating its 160th anniversary this year. In 1857 its founders envisioned that the magazine would “honestly endeavor to be the exponent of what its conductors believe to be the American idea.” In the current issue one of its writers asks, “Is the American Idea Doomed?” and claims that it has few supporters on either the left or the right. Well, I happen to be in the middle and I think the American idea is doing very well indeed.

Consider:

Consider:

- The World Economic Forum ranks the U.S. as the world’s most competitive large economy and, in fact, the U.S. is getting richer faster than anybody else.

- Productivity growth in the digital industries has grown at the annual rate of 2.7% over the past 15 years compared with only an anemic .7% annual growth in productivity in the physical industries. The U.S. economy is becoming more digital all the time.

- The four U.S. companies, Amazon, Apple, Facebook and Google are in the process of revolutionizing all aspects of life not only in America but all around the world.

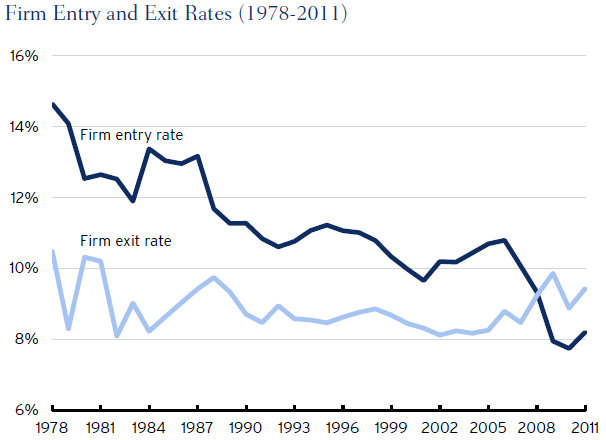

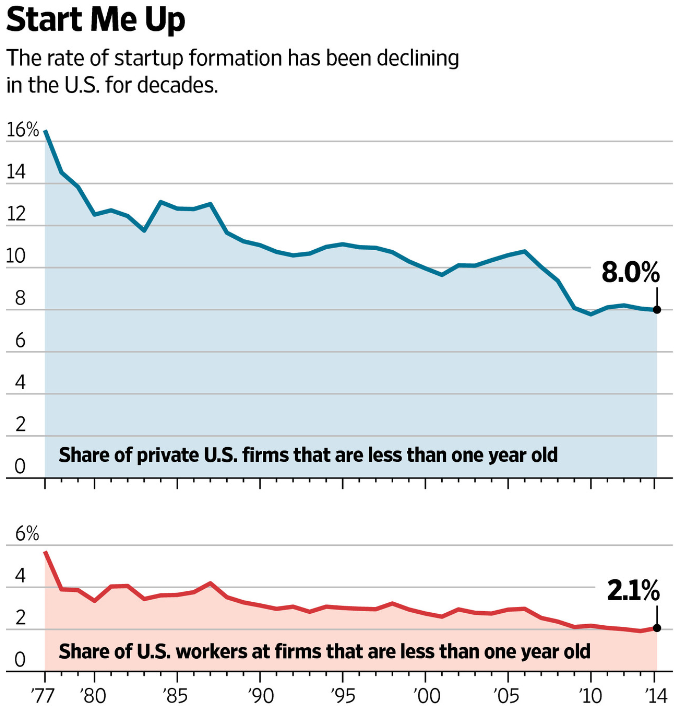

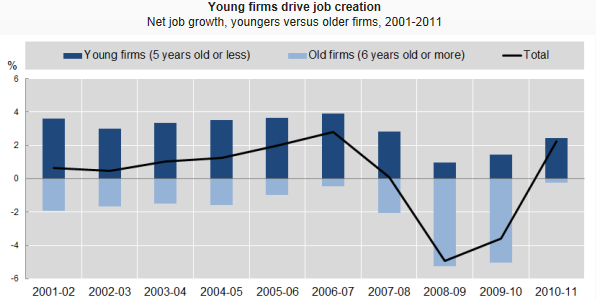

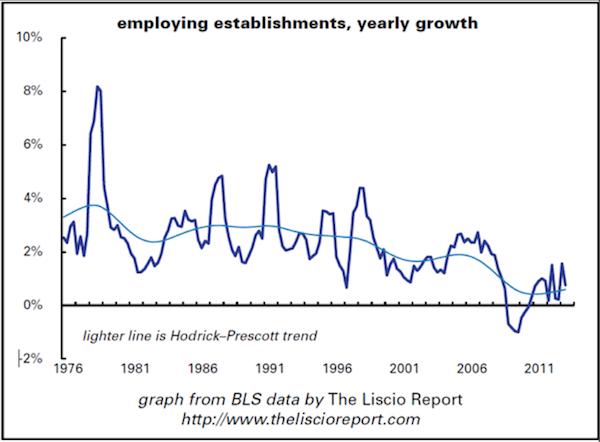

- According to the Kauffman Foundation entrepreneurship is flourishing in the U.S. (see chart), and not just in Silicon Valley.

- According to Freedom House democracy has made much progress around the world in the last 30 years, even if further growth has stalled for the past ten years. Other democratic countries are our best friends and so we want more of them.

- Granted Donald Trump is a wild card. So far his record is mixed but he hasn’t made any big mistakes (liking dragging us into war or hurting the economy). It is unlikely that he’ll slow our huge forward momentum whether or not he helps it.

Conclusion. “The democratic experiment is fragile” (perhaps!) but it’s also got a lot going for it right now. We can never afford to be complacent but we need not be pessimistic either.