In a recent post I discussed the issue of slow economic growth in the U.S. and why it is so harmful and dangerous to our nation’s future. In short, it not only deprives many citizens of a more prosperous life and makes it more difficult to shrink our annual budget deficits, but it also endangers our national security as our chief competitor, China, grows faster than we do.

In the long run, an economy can expand only at a rate sustained by the growth of its labor force and the productivity of its workers. I have previously pointed out that there are far too many prime working age men who are unemployed.

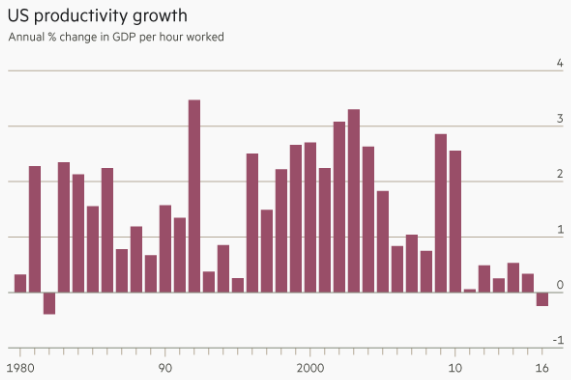

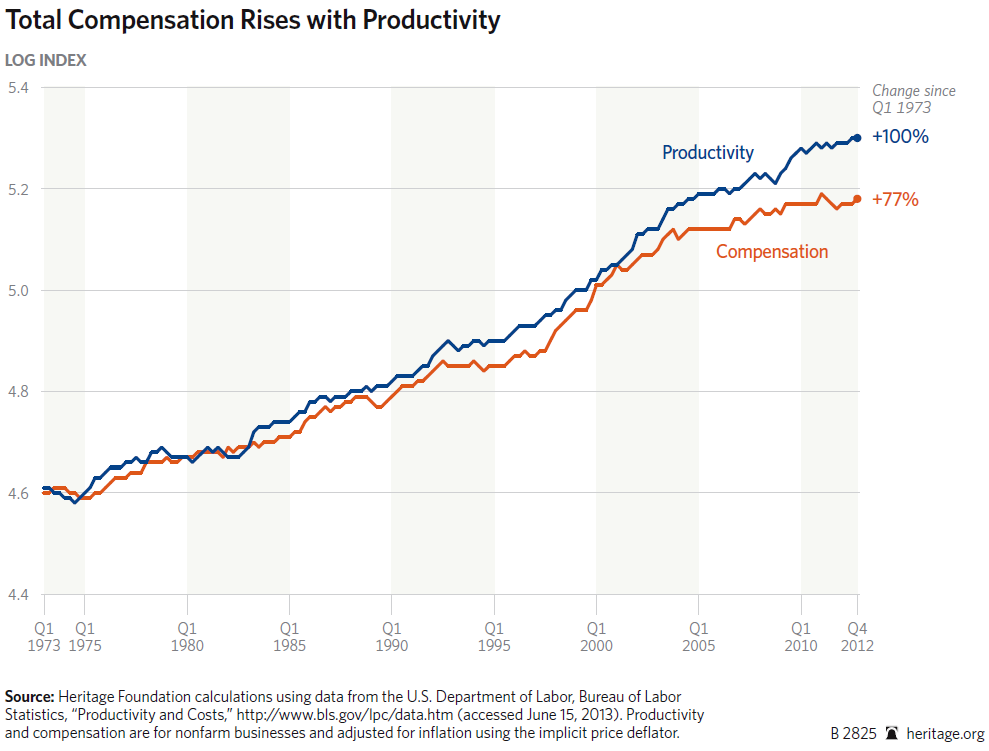

Today let’s talk about the rate of productivity growth (see the above chart). In particular:

Today let’s talk about the rate of productivity growth (see the above chart). In particular:

- From 1994 – 2003, U.S. output per hour worked rose annually by an average of 2.8%. Since then it has grown at an annual rate of 1.3%, including just 0.4% since 2011.

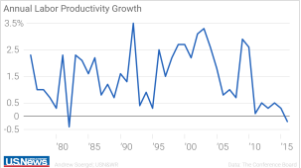

- Business capital spending is down as companies are spending their profits to buy back stock rather than making new investments (see second chart).

As I have previously discussed, the U.S. is now caught in a vicious trap:

As I have previously discussed, the U.S. is now caught in a vicious trap: - Slow growth keeps the under-employment level (U6) high and also means minimal raises for employed workers The resulting economic slack leads to

- Low Inflation. But low inflation in turn means that the Federal Reserve can maintain

- Low Interest Rates to try to encourage borrowing. But an unfortunate side effect of low interest rates is that Congress can borrow at will and run up huge deficits without really having to worry about paying interest on this “free” money. This leads to

- Massive Debt. But what is going to happen when inflation does eventually take off and the Fed is forced to raise interest rates? Then we will be stuck with huge interest payments on our accumulated debt. When this happens, interest payments plus ever growing entitlement spending will eat up most, if not all, of the federal budget. This will inevitably lead to a severe

- Fiscal Crisis.

Conclusion. It is absolutely imperative to speed up economic growth.

Follow me on Twitter

Follow me on Facebook

{kind=link}