The Congressional Budget Office has a sterling reputation for collecting accurate data and making credible predictions about basic economic and fiscal trends. CBO analyses, which are based on current law, are generally accepted as valid by both liberals and conservatives. Considering the degree of hyper-partisanship in most discussions of fundamental policy, it is reassuring to at least have an unimpeachable source of basic information.

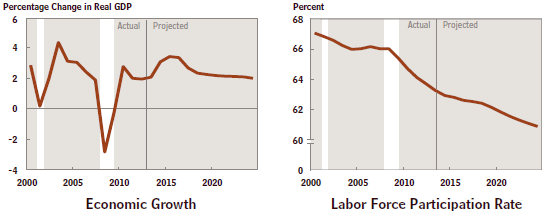

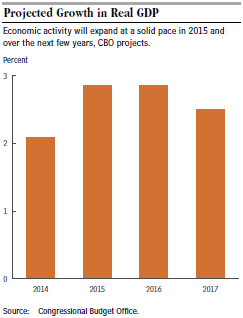

CBO has just released its regular annual report, ”The Budget and Economic Outlook: 2015-2025.” There is good news for the near term. As shown above, GDP is projected to grow by 2.9% in the (budget) years 2015 and 2016, and dropping to 2.5% growth in 2017, which is still better than 2014. This means that our national debt will not grow from its current level of 74% of GDP for the next few years and might even decrease slightly.

CBO has just released its regular annual report, ”The Budget and Economic Outlook: 2015-2025.” There is good news for the near term. As shown above, GDP is projected to grow by 2.9% in the (budget) years 2015 and 2016, and dropping to 2.5% growth in 2017, which is still better than 2014. This means that our national debt will not grow from its current level of 74% of GDP for the next few years and might even decrease slightly.

Growth will then hover around 2.2% for the remainder of the 2015 – 2025 decade, which is the average GDP since the end of the Great Recession in June 2009. Likewise, unemployment will likely not fall much below its current value of 5.6% for the next ten years. In short, under current policy, except for the next couple of years, we are stuck in the same slow-growth rut where we have been for the past five and one-half years.

Growth will then hover around 2.2% for the remainder of the 2015 – 2025 decade, which is the average GDP since the end of the Great Recession in June 2009. Likewise, unemployment will likely not fall much below its current value of 5.6% for the next ten years. In short, under current policy, except for the next couple of years, we are stuck in the same slow-growth rut where we have been for the past five and one-half years.

It should be obvious that we need new policies to speed up growth, put more people back to work, and raise the stagnant wages endured by many middle- and lower-income workers. How can this be accomplished?

- Tax reform, both individual and corporate, is the primary route to faster growth. Lower tax rates across the board, paid for by closing loopholes and shrinking deductions. This will put extra income in the pockets of the 64% of taxpayers who do not itemize deductions, which they will likely spend. It will also make it easier for potential entrepreneurs to successfully launch a new business.

- Immigration reform, expanded foreign trade and deregulation will also create more business opportunities which will in turn grow the economy and create more jobs.

Hopefully the new Congress will be able to move forward in this direction. A better future depends on it!