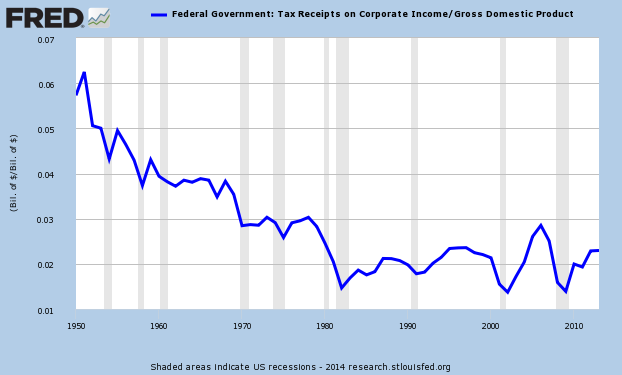

It is a very good idea to cut the top corporate tax rate to 20% or so from its current 35% level. This will make the U.S. competitive with other developed countries and encourage our multinational companies to bring their foreign profits back home for reinvestment in the U.S. It will also encourage other foreign companies to set up shop in the U.S.

My last post, however, strongly criticizes the current GOP tax plan, now in Conference Committee, because it will add $1 trillion to our already huge debt:

- Current national debt, at 77% of GDP (for the public part on which we pay interest) is the highest it has been since right after WWII, and is already predicted by CBO to keep getting worse, without major changes in current policy. When interest rates eventually return to more normal and higher levels, interest payments on the debt will skyrocket. And this will continue indefinitely, eventually leading to a new fiscal crisis, much worse than the Financial Crisis of 2008.

This means that the GOP tax plan, by adding an additional $1 trillion to our debt, is terrible fiscal policy. But the situation is even worse than this. It is also bad economic policy:

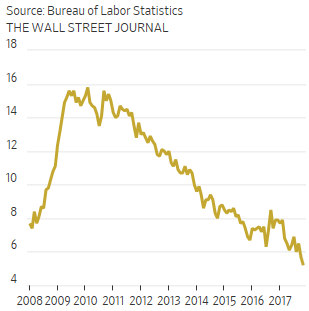

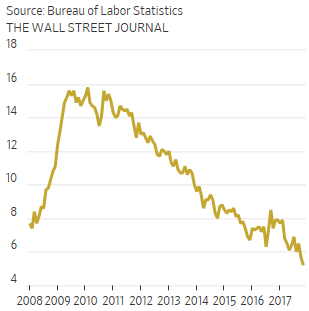

- Economic growth is finally becoming robust. We now have had two quarters in a row of 3% growth. In 2015 median household income grew by 5.2% with another 3.2% added in 2016. Blue collar wages are beginning to take off (see chart). The overall unemployment rate has dropped to 4.1%. Even the unemployment rate for Americans age 25 and older, without a high school diploma, has dropped to 5.2% (see second chart).

Conclusion. The last thing our economy needs right now is the artificial stimulus caused by a deficit-financed tax cut. It is likely to overheat an already hot economy and thereby ignite inflation which will force the Federal Reserve to raise interest rates much faster than would otherwise be necessary.

Follow me on Twitter

Follow me on Facebook