The Republican tax plan has many good features and is now moving along in Congress. The best feature of all is reducing the top corporate rate from 35% to 20%. This will make the U.S. internationally competitive and create a strong incentive for all multinational companies to conduct more business in the U.S. and for U.S. multinationals to bring their profits back home for reinvestment.

The Tax Foundation estimates that the Senate version of the Plan will lead to the creation of 925,000 new jobs and an after tax income gain of $2,598 for a middle-income family over a ten year period.

But there are several parts of the plan which could be significantly improved. For example:

- Revenue neutrality, at least on a dynamic basis (taking growth into account) is essential. Our national debt is way too large to ignore.

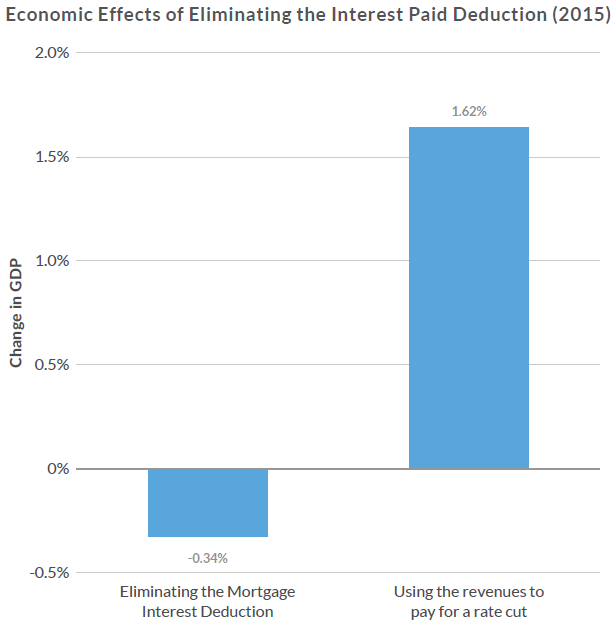

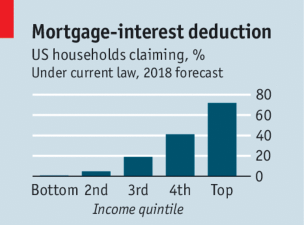

- Shrinking more deductions, to achieve revenue neutrality. The mortgage interest deduction should be eliminated completely, not just limited to $500,000 mortgages. Same for the state and local tax deduction.

- More progressivity. Keep the estate tax to bring in more tax revenue. Scrap the lower 25% rate for a pass-through business tax because it will be too easy to abuse. The Congressional Budget Office has estimated that eliminating the individual mandate for the ACA will save $338 billion over ten years. It will also save millions of Americans from having to pay a tax penalty of $695 or more for not having health insurance.

- Emphasis on growth. Make expensing (i.e. immediate write-off) for new investment a permanent feature rather than limited to five years only.

Conclusion. There are lots of good features in the Tax Reform Plan. Several changes would make it even better. As soon as it achieves stability in the legislative process, the CBO will analyze its fiscal and economic effects. At this point revenue neutrality will be essential for achieving broad support.