I voted for Hillary Clinton last November. Not because I liked her program. I was voting against Donald Trump. He is crude, sleazy and a terrible narcissist. I preferred John Kasich, Governor of Ohio, in the Republican Primary. But he didn’t make it. I voted for Mitt Romney in 2012 but he didn’t make it either.

The question now is whether or not the Trump Administration will effectively address our country’s two biggest problems, both of which are very serious and need urgent attention:

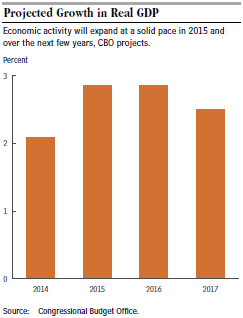

- Slow economic growth, averaging just 2% per year since the end of the Great Recession in June 2009. Faster growth means a tighter labor market which in turn means more workers and higher wages. This in turn means less inequality. Furthermore, it is the United States’ dominant economic strength which assures world peace and stability. The Chinese economy, now half the size of ours, will catch us eventually. But stronger U.S. growth will delay this and enable us to cope with it better when it happens.

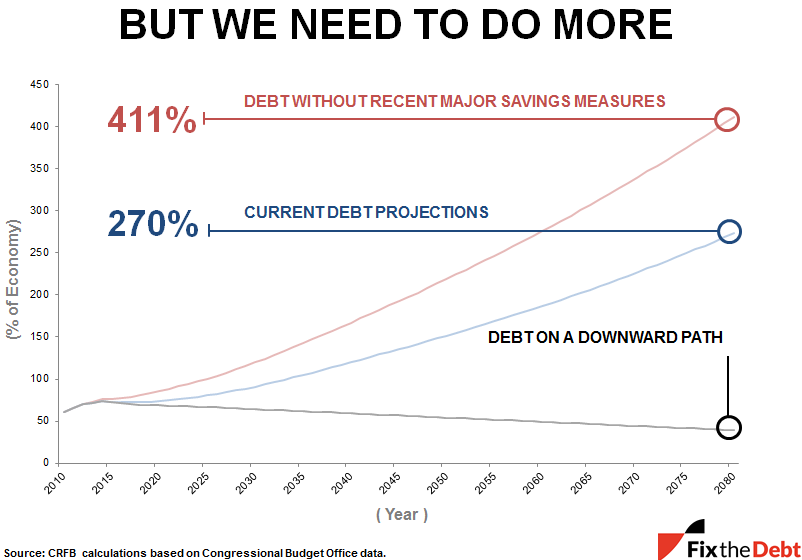

- Massive Debt. The public debt of $14 trillion (on which we pay interest) is now 77% of GDP, (https://itdoesnotaddup.com/2017/01/31/trump-needs-a-wall-of-fiscal-discipline/) the highest since the end of WWII and steadily getting worse. With current low interest rates the debt is now essentially “free” money. But what will happen when interest rates return to normal historical levels? At this point interest payments on the debt will rise precipitously and become a huge drain on the budget. We can’t prevent this from happening but we can lessen the impact by acting now.

Will the Trump Administration take these two problems seriously?

- For sure on economic growth. His re-election chances in four years depend largely on the fortunes of his base of blue-collar workers. His appointments at Treasury (Mnuchin), HHS (Price), and EPA (Pruitt) all support the tax reform and deregulation needed to get this done. I am confident that Trump will avoid a disastrous trade war.

- The debt. This is trickier because Trump has said he won’t touch Social Security or Medicare. My optimism is based on the fact that the Debt Ceiling will be re-imposed on March 16 at its level on that date. This will give Congress just a few months to raise the ceiling to a higher level. It is likely that the many fiscal conservatives in the House will insist, in return, for some sort of spending restraint such as a ten-year plan to balance the budget.

Conclusion. We’re not out of the woods yet. But there is a clear path showing the way forward.

Follow me on Twitter

Follow me on Facebook