My last post is highly critical of the economist and New York Times columnist, Paul Krugman, for encouraging massive new deficit spending to stimulate our under-performing economy.

Debt and the slow growth of our economy are the two main topics of this blog which I have now been writing for almost four years. How to speed up growth is a complicated and highly charged political issue about which reasonable and well informed people can differ. However avoiding excessive debt is to me a moral issue whose resolution should not be that difficult, at least in a conceptual sense.

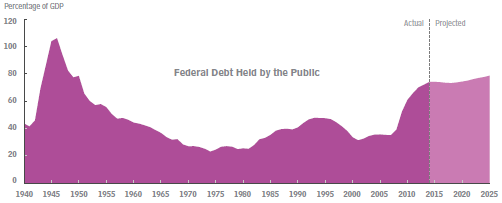

I have often used the above chart from the Congressional Budget Office to illustrate our debt problem because it clarifies the problem so vividly. Here are its main features:

I have often used the above chart from the Congressional Budget Office to illustrate our debt problem because it clarifies the problem so vividly. Here are its main features:

- Our public debt (on which we pay interest), now about $13 trillion, is 75% of GDP, the highest since right after the end of WWII. And it is projected to keep getting steadily worse under current policy.

- Note the decline in the debt from the end of WWII until about 1980. This doesn’t mean that the debt was actually paid off but rather that it shrank as a percentage of GDP as the economy grew fairly rapidly during this time period.

- From 1980 – 2008 the debt level fluctuated and increased somewhat but did not get badly out of control.

- Debt shot up rapidly with the Great Recession and has been continuing to grow ever since.

- The current GDP of our economy is about $19 trillion. At a current growth rate of 2.1%, this adds $400 billion of GDP per year. This means that a $400 billion deficit for 2016 would stabilize the public debt at 75% of GDP. But our 2016-2017 deficit is projected to be almost $600 billion (and rising). This is not good enough!

Conclusion. In order to begin to shrink the size of the public debt, it is imperative that annual spending deficits be reduced to well below $400 billion per year. This will be difficult for our political process to achieve but it is the only way to avoid a new and much worse financial crisis in the relatively near future.