I seldom use the New York Times sociological columnist, David Brooks, as a source for my blog posts because I am focused primarily on economic and fiscal issues. But his column today, “Saving The System,” is highly pertinent to my message.

“All around, the fabric of peace and order is fraying. The leaders of Russia and Ukraine escalate their apocalyptic rhetoric. The Sunni-Shiite split worsens as Syria and Iraq slide into chaos. China pushes its weight around in the Pacific. … The U.S. faces a death by a thousand cuts dilemma. No individual problem is worth devoting giant resources to. But, collectively, all the little problems can undermine the modern system.”

“All around, the fabric of peace and order is fraying. The leaders of Russia and Ukraine escalate their apocalyptic rhetoric. The Sunni-Shiite split worsens as Syria and Iraq slide into chaos. China pushes its weight around in the Pacific. … The U.S. faces a death by a thousand cuts dilemma. No individual problem is worth devoting giant resources to. But, collectively, all the little problems can undermine the modern system.”

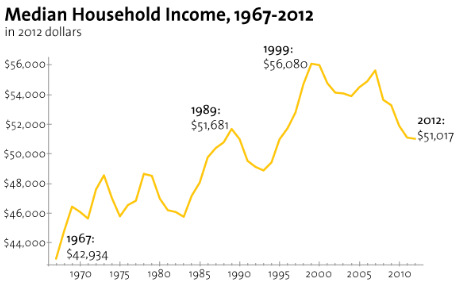

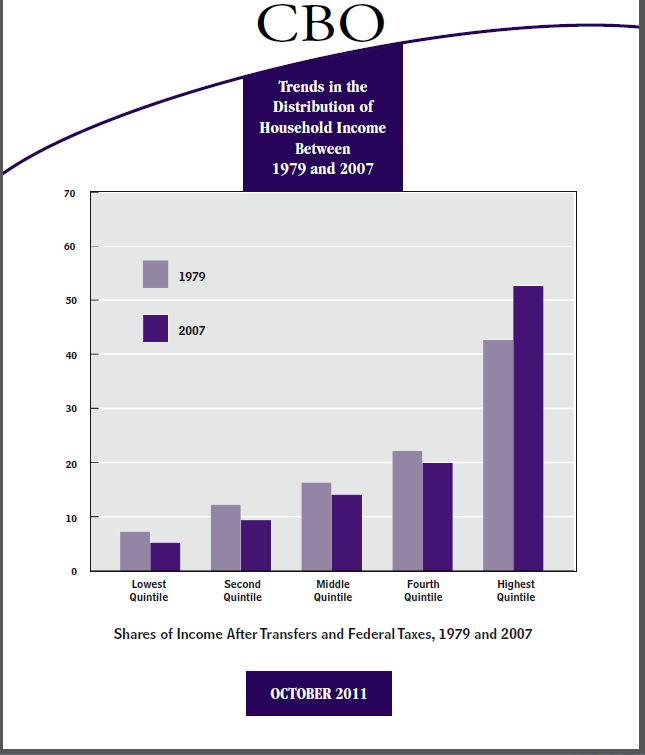

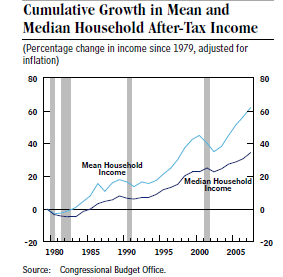

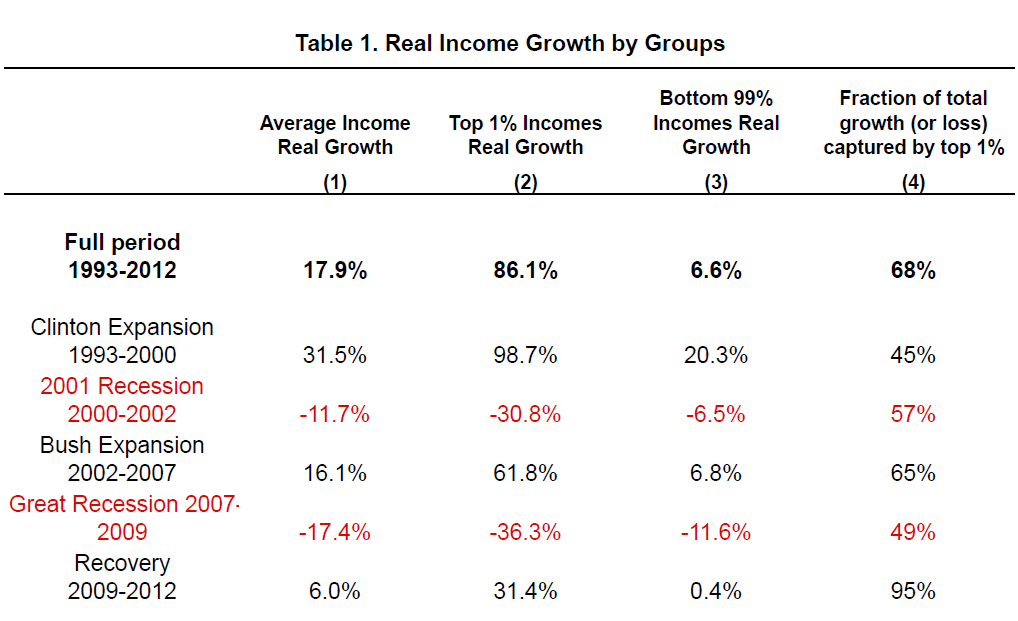

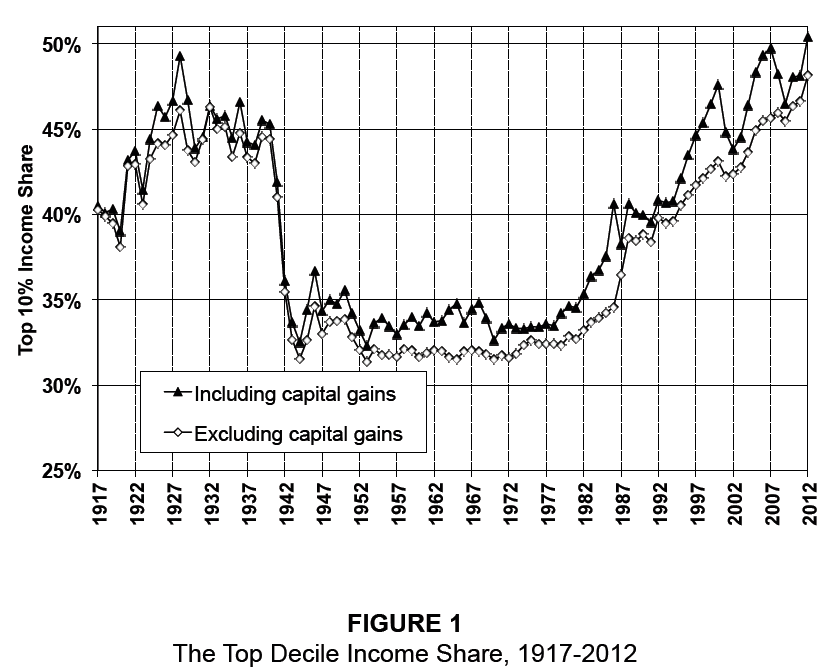

In addition to all of these pesky worldwide problems, our free enterprise economic system is under siege. Wages have been largely stagnant since the early 1970s and income inequality is growing as the top 1%, and perhaps the top 10 or 15% as well, do much better than everyone else. And just lately we have also learned from the French economist, Thomas Piketty, that wealth inequality has been growing steadily ever since about 1950 and is likely to get substantially worse in the future.

In other words, western civilization is under threat in more ways than one. What are we going to do about it? At the risk of oversimplifying, I believe that the single best thing we can do is to undertake fundamental tax reform to make our economy stronger. Cut everyone’s tax rates and pay for it by closing loopholes and deductions which primarily benefit the wealthy.

- Lower tax rates will put more money in the hands of the two thirds of Americans who don’t itemize their tax deductions. These are largely the same people with stagnant wages and so they will spend this extra income they receive.

- The resulting increase in demand will put millions of people back to work and thereby increase tax revenues which will help balance the budget. This shift of income from the wealthy to the less wealthy will reduce income inequality.

- Although harder to implement politically, a low (between 1% and 2%) wealth tax on financial assets above a threshold of $10 million per individual, would be a highly visible way to address wealth inequality. The substantial sum of revenue raised by this method could be used to fund national priorities as well as paying down the deficit.

I don’t want to leave the impression that I consider this program to be a panacea for strengthening our country. But it would help and we need to make some big changes to maintain our status as world leader.