It is widely recognized and deplored, see here and here, that economic growth in the U.S. has been very slow, averaging only 2% per year, since the end of the Great Recession in June 2009.

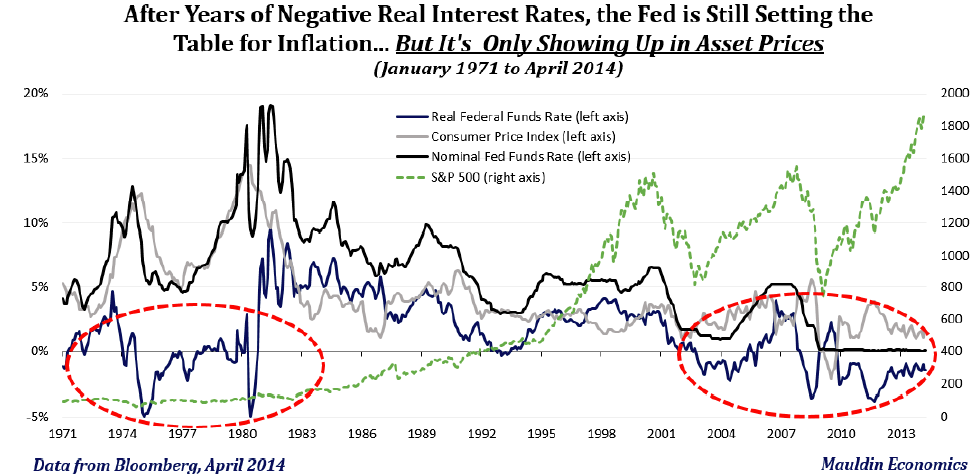

The Federal Reserve has taken unprecedented steps to limit the severity of the recession by holding down both short term and long term interest rates. But these efforts are only partially working and are, unfortunately, having a number of negative effects as well.

It also has been made quite clear that the problem is supply side and not demand side. This is because, on the one hand, wages are beginning to rise more quickly and consumers are spending more money but, on the other hand, business investment is shrinking which is leading to slow productivity growth.

The American Enterprise Institute’s James Pethoukoukis has just provided new data on the current weakness of business investment as illustrated in the above chart. Furthermore he quotes the economist, Robert Gordon, who has clearly described the many headwinds holding back the U.S. economy to the effect that:

The American Enterprise Institute’s James Pethoukoukis has just provided new data on the current weakness of business investment as illustrated in the above chart. Furthermore he quotes the economist, Robert Gordon, who has clearly described the many headwinds holding back the U.S. economy to the effect that:

“The American tax code exerts a downward pressure on capital formation and therefore on economic growth. It is now 30 years since the passage of comprehensive federal tax reform in the U.S. In the intervening years, nearly every developed country has reformed its tax codes to make them more competitive than that of America. Meanwhile the U.S. has allowed its tax code to atrophy.”

Conclusion. Yes, economic growth can be speeded up. But monetary policy won’t do the trick. Congress must intervene with the right changes to fiscal policy, i.e. lowering tax rates for both individuals and corporations, paid for by closing loopholes and shrinking deductions.