My last post, “The Big Picture on America’s Fiscal Crisis” explains, according to the political scientist James Piereson, why three very difficult contemporary problems:

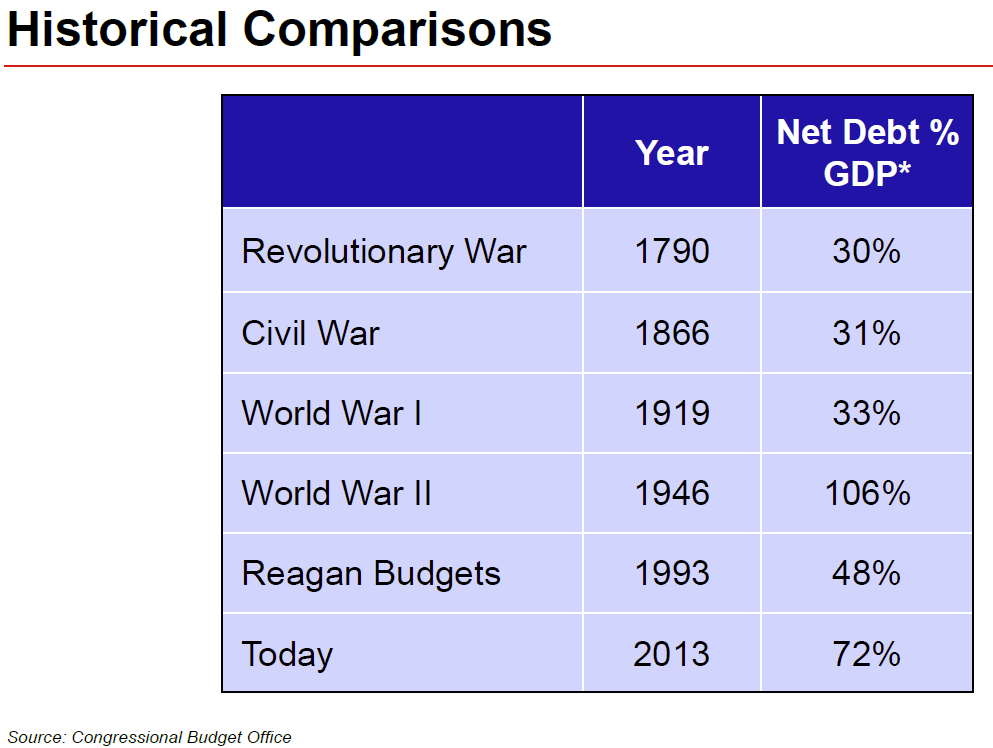

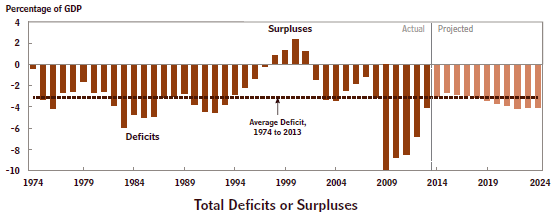

- Very high public debt (74% of GDP, highest since WWII)

- Unfavorable demographics (a rapidly increasing number of retirees)

- Slowing economic growth (for fundamental reasons)

will inexorably lead to a breakdown of the Democratic-welfare regime which has lasted from 1932 until the present. The reasoning is very simple and direct. We already have huge debt. Rapidly increasing entitlement spending on our rapidly increasing number of retirees will keep driving our debt higher and higher. We won’t be able to grow our way out from under this debt because we have run out of industrial revolutions to spur new growth.

A new study co-written by Doug Elmendorf, CBO Director from 2009-2015, makes the case that our fiscal crisis, although real, is less urgent than often believed for the following reasons:

A new study co-written by Doug Elmendorf, CBO Director from 2009-2015, makes the case that our fiscal crisis, although real, is less urgent than often believed for the following reasons:

- Lower than expected health-care inflation

- The persistence of low interest rates

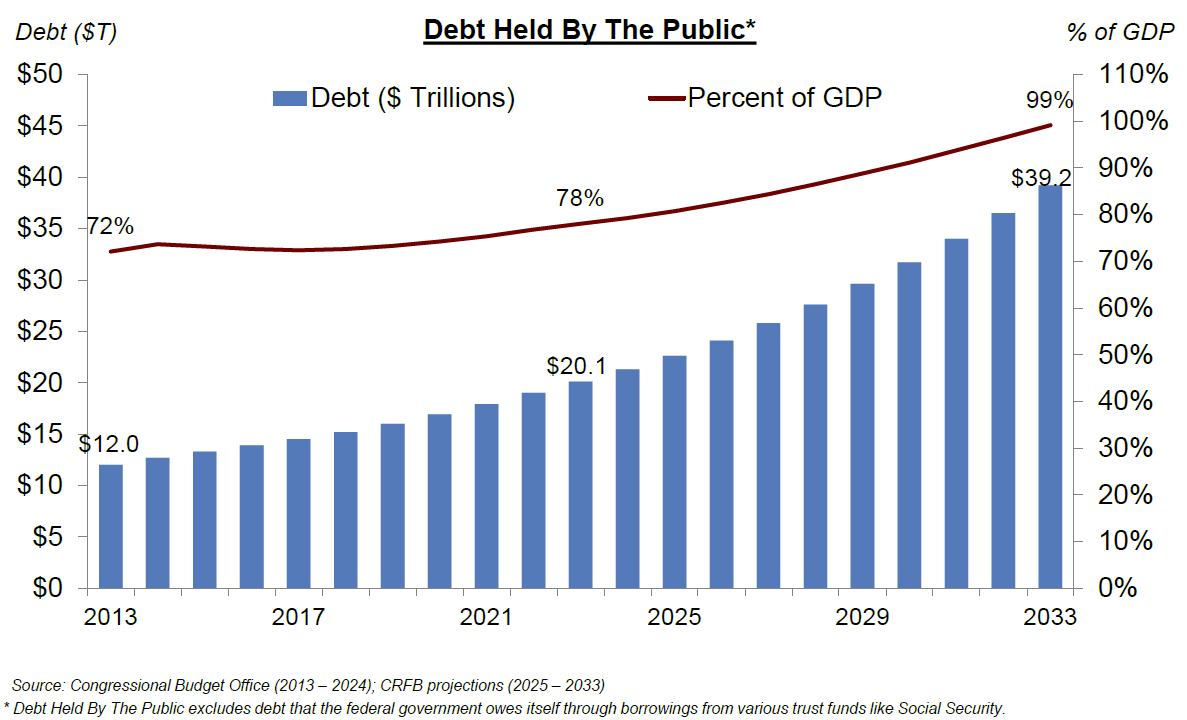

The above chart shows, for example, that the public debt may not reach 100% of GDP until 2032 instead of the earlier CBO prediction of 2030. I believe that this Elmendorf projection should be viewed as false comfort.

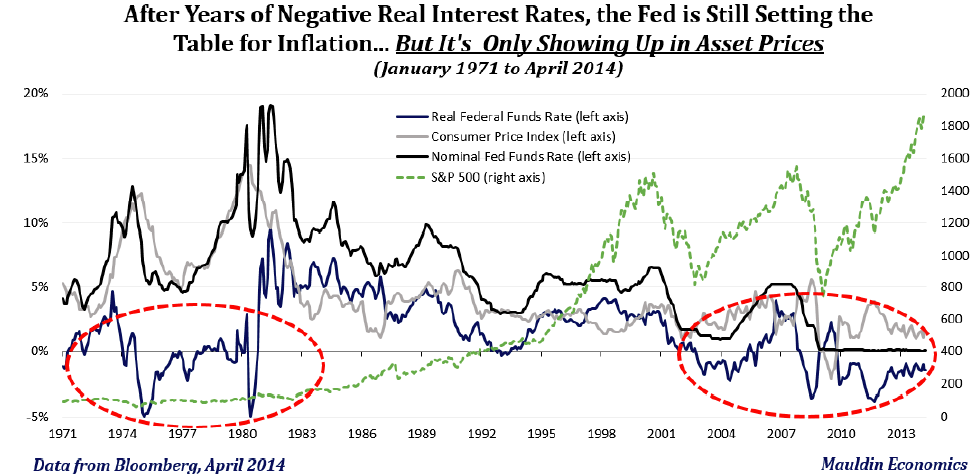

Both health-care inflation and low interest rates are a direct result of very low overall inflation in the U.S. and this will not last forever. Low interest rates mean that interest payments on the debt are also very low. This is a very poor reason to increase current borrowing. When interest rates do go up, whether it is sooner or later, interest payments on the debt will increase by hundreds of billions of dollars a year over a likely relatively short time period.

This is the severe crisis, or Fourth Revolution, which Mr. Piereson is predicting. We don’t know when it will occur because we don’t know when inflation will rear its ugly head.

Wouldn’t it be much better to put our debt on a downward path, as a percentage of GDP, and avoid the otherwise very unpleasant consequences?

Follow me on Twitter: https://twitter.com/jack_heidel

Follow me on Facebook: https://www.facebook.com/jack.heidel.3