Americans are a very fortunate people. We are protected by two oceans and friendly neighbors to our north and south. We are the strongest country in the world, both economically and militarily. We provide the world with cutting edge leadership in many areas such as technology, finance, energy production, scientific research and university education.

In short we live in a very successful, prosperous and complex society. We do have serious problems but they are being addressed by our elaborate legal and governmental processes and structures. Slowly but surely life in America is getting better and better all the time.

Given our country’s size, complexity and dominance in the world, it is inevitable that government will also grow in size and structure in order to take on new responsibilities. It is completely unrealistic to think that we can return to a more limited form of government that existed in the past.

When I say, then, that I’m a fiscal conservative, I am not advocating for less government but merely that we pay for the government that we have, in other words, act in a fiscally responsible manner.

And we are not doing this at the present time:

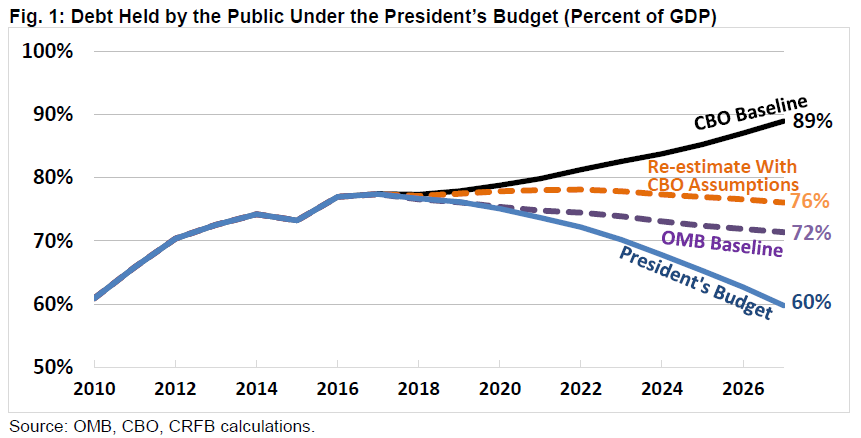

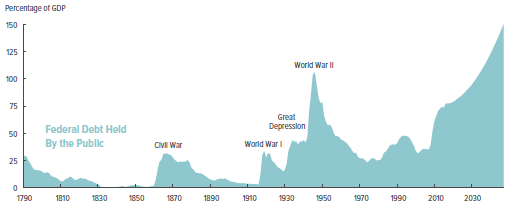

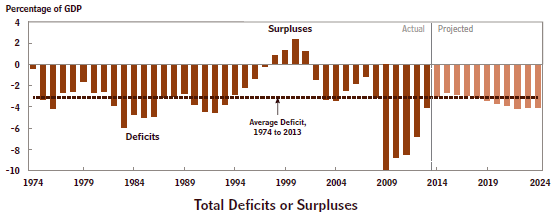

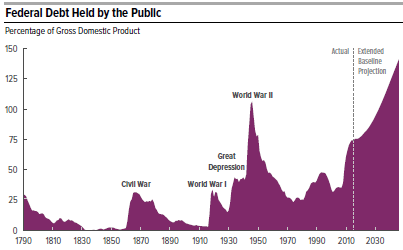

- Our national debt, now 77% of GDP (for the public debt on which we pay interest), is the highest since right after WWII. It is predicted by the Congressional Budget Office that it will keep steadily getting worse without major changes in current policy.

- The urgency of the debt problem is based on the fact that interest rates are now so low that it is almost “free” money. But interest rates will inevitably return to more normal historical levels and, when this happens, interest payments on the debt will skyrocket. Eventually this will lead to a Fiscal Crisis, much worse than the Financial Crisis of 2008.

- The solution to this problem need not be drastic. Federal spending is growing by 5% per year while tax revenues are growing by 3% per year. If we would just hold spending increases down to 2.5% per year, the federal budget would be balanced in a few years and our debt would start shrinking as a percentage of GDP.

Conclusion. Spending restraint, with very few actual spending cuts, is all that it will take to put our debt problem on a path to solution. Surely we are capable of acting in a fiscally responsible manner like this!