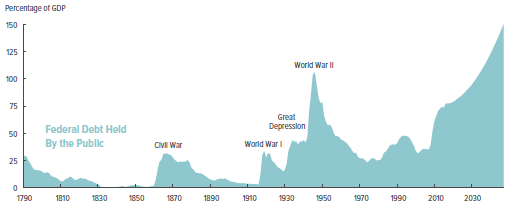

So declared Douglas Holtz-Eakin, former director of the Congressional Budget Office, in March 2011. At the time, federal debt held by the public (on which we pay interest) stood at 63% of GDP. Now, just six years later, that ratio stands at 77% and is projected by the CBO to reach 150% by 2047 if current laws remain unchanged.

The CBO has just released its latest (March 2017) report and the debt situation continues to get worse:

- The interest rate on federal debt has averaged 5.8% over the past 60 years. It is now at an unusually low 2% and the CBO projects that it will climb no higher than 4.4% by 2047. Even with such a conservative projection, the total cost of servicing the debt will rise to almost 1/3 of federal revenue by 2047, compared with just 8% today.

Here are some of the dire consequences of such a large and growing debt:

- Reduces national savings and income in the long term because more of people’s savings would be used to buy Treasury securities, thus crowding out private investment.

- Increases the government’s interest costs and thus makes it much more difficult to lower deficits.

- Reduces the ability to respond to unforeseen events. For example, when the Financial Crisis hit in 2008, public debt stood at 40% of GDP and lawmakers had the flexibility to respond to the crisis with both TARP and a fiscal stimulus. Such costly actions will be much more difficult next time.

- Increases the chances of a new fiscal crisis if investors become less willing to finance more federal borrowing or demand higher interest rates in return.

Conclusion. The more debt that accumulates and the higher interest rates rise, the more painful it will become to implement a solution. What is really scary is that nothing will be done until a new crisis occurs. Then we will be forced to act and it will be very painful indeed.