Based on a post I wrote last fall, “Solving the Student Debt Problem,” and a recent Op Ed by the economics journalist, Robert Samuelson, “Good News on the College Debt Front,” here is where I think we are on this serious problem:

- The unemployment rate is very low for college graduates, about 2.5%. We should strongly encourage post-secondary education for all.

- Since 1996 outstanding student loans have risen from $200 billion to $1.3 trillion.

- Counting both community colleges, four year colleges and universities, 56% of college students borrow money to pay for college costs.

- For undergraduates who attended two and four year colleges, more than half of loans were less than $20,000. Only 10% exceeded $40,000.

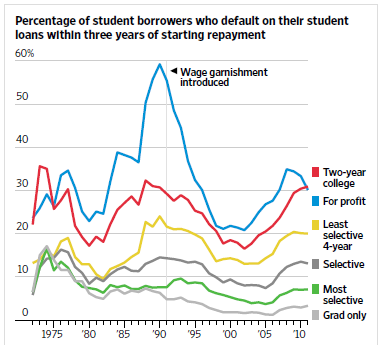

- The highest default rates occur at community colleges (23% in 2012) and at for-profit colleges (18%). Hurt worst are low-income and minority students who never graduated but have unpaid debts.

- The Federal Reserve Bank of New York has found a close correlation between subsidized loan and Pell Grant limits and the rapid increase of college tuition costs.

It seems clear that the way to address this problem is to focus on where it is worst: for the low-income and minority students who attend community colleges and for-profit colleges.

In other words:

In other words:

- Place a strict lid on the total amount of subsidized loans available for undergraduates, say $25,000 to $30,000 per person.

- Use the savings achieved in doing this to increase the size of Pell grants for the lowest income students who need help the most.

- Overall faster economic growth will help college graduates and dropouts alike find better paying jobs and make it easier for them to pay back their college debts.

- On an individual basis, urge all students, but especially low-income and minority students, to avoid debt as much as possible in the first place!

Conclusion: Careful analysis of the student debt problem shows that there are very useful steps to take which will not cost the federal government more money.