Every Monday and Friday morning when I pick up the New York Times, I immediately turn to the OP-ED page to see what liberal icon Paul Krugman is saying. In his most recent column, “Debt Is Good,” he says that “what ails the world economy right now is that governments aren’t deep enough in debt.”

Here is my response to his argument:

Here is my response to his argument:

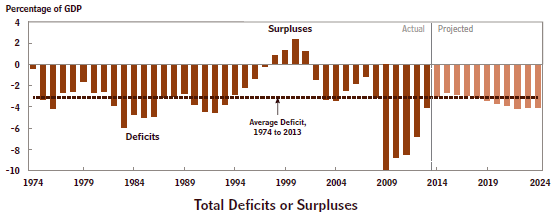

- “The federal government can (now) borrow at historically low interest rates. So this is a very good time to be borrowing and investing in the future.” Our public debt (on which we pay interest) is now $13 trillion or 74% of GDP, the highest since the end of WWII, as shown in the above chart from the Congressional Budget Office. It is likely that interest rates will soon begin to go up. Every 1% rise will increase interest payments on our already existing debt by $130 billion per year. Where are the hundreds of billions of new dollars for debt service going to come from in an already tight budget? The more we add to the debt, the worse this problem will become.

- “Having at least some government debt helps the economy function better.” I agree! But $13 trillion is way beyond what is needed for this. It is outrageously excessive!

- “What we need are policies that would permit higher (interest) rates in good times without causing a slump. And one such policy would be targeting a higher level of debt.” The problem here is the conceit of Keynesians, like Mr. Krugman, that monetary policy alone can restore us to economic and fiscal health. Rather than accepting that the economy has entered a “new normal” with a permanently slow growth rate of about 2% (as has been the case since the end of the Great Recession in June 2009), we need policy changes such as individual and corporate tax reform (revenue neutral to be sure) and changes in the Affordable Care Act and Dodd-Frank Act to remove their job killing features.

Anybody with an ounce of common sense knows that excessive borrowing will eventually lead to disaster. Mr. Krugman seems to think that by constantly ridiculing his opponents, he can get away with denying this simple truth.