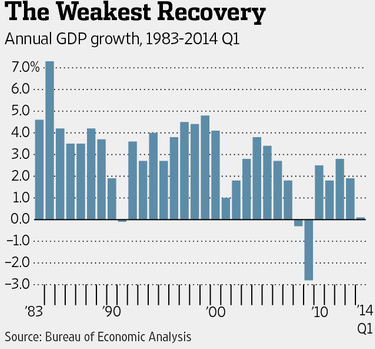

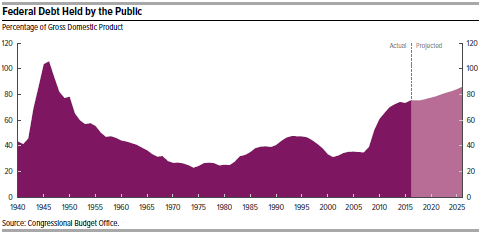

As regular readers of It Does not Add Up know well, I am highly alarmed about the large budget deficits and slow economic growth in the U.S. in recent years. Some people respond that deficits are falling and that we have entered a new era of slow-growth secular stagnation which is unavoidable.

A new report from the Congressional Budget Office, our most reliable source for objective fiscal and economic information, now predicts that the deficit for 2016 will be $544 billion, a large increase over the $439 billion deficit for 2015. Furthermore, CBO predicts that for future years deficits will continue to grow, exceeding $1 trillion by 2022. Here is a summary of the CBO predictions:

A new report from the Congressional Budget Office, our most reliable source for objective fiscal and economic information, now predicts that the deficit for 2016 will be $544 billion, a large increase over the $439 billion deficit for 2015. Furthermore, CBO predicts that for future years deficits will continue to grow, exceeding $1 trillion by 2022. Here is a summary of the CBO predictions:

- Federal outlays are projected to rise by 6% this year, to $3.9 trillion, or 21.2% of GDP. This represents a 7% rise in mandatory (entitlement) spending, a 3% increase in discretionary spending, and a 14% increase in net interest on the national debt.

- Under entitlements, Social Security payments will increase by 3% and healthcare (Medicare, Medicaid, CHIP (children’s health) and Obamacare) payments will increase by 11%.

- Revenues will increase by 4% in 2016, to $3.4 trillion, or 18.3% of GDP.

- Deficits are projected to increase from 74% of GDP in 2015 to 86% of GDP by 2026.

- Spending for mandatory programs will increase from 13.1% of GDP in 2016 to 15% of GDP in 2026.

First Conclusion: The spending increases from 2015 to 2016, outlined above, illustrate a clear and alarming trend which is evident in the full ten-year set of CBO data. Discretionary spending will rise but at a sustainable rate of about 3% a year or less. Mandatory (entitlement) spending will rise at a much faster and unsustainable rate. It is healthcare spending, i.e. for Medicare, Medicaid, CHIP and Obamacare, and not Social Security, which is driving the rapid increase in mandatory spending.

Second Conclusion: Although it is government healthcare spending which is driving our rapidly worsening deficit and debt problem, this is just part of the larger problem of the rapidly increasing cost of overall (including private) healthcare spending in the U.S. This is the basic problem we need to focus on to get both fiscal and economic policy back on the right track.

Follow me on Twitter: https://twitter.com/jack_heidel

Follow me on Facebook: https://www.facebook.com/jack.heidel.3