It is now commonly agreed that the Financial Crisis of 2008 was caused by the collapse of the housing bubble beginning in 2007. There were three main aspects to the huge collapse of wealth caused by the Financial Crisis:

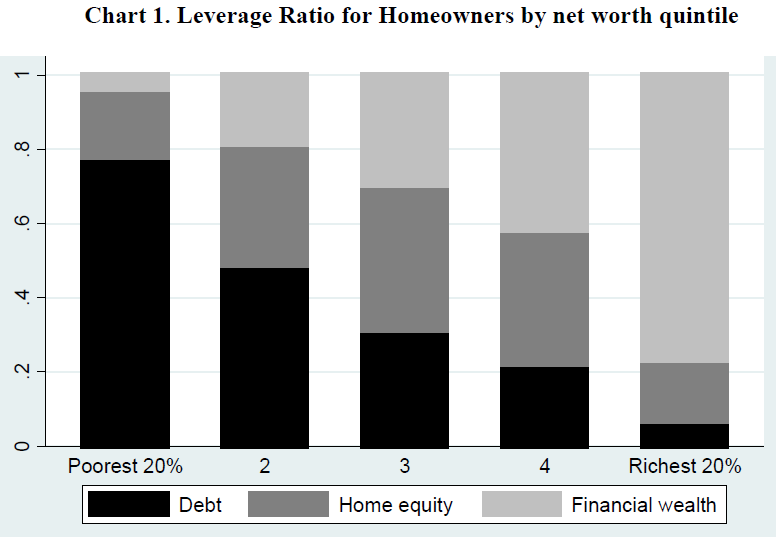

- It Destroyed Mainly Middle Class Wealth. During the Great Recession housing values collapsed by $5.5 trillion, a large fraction of the total $14 trillion economy. As shown in the above chart, most of this loss of wealth came at the expense of middle- and lower-income families.

- Foreclosures on Underwater Mortgages Lowered Housing Values across the Board. When foreclosed houses are sold at steeply discounted prices, the appraised value of all other houses in the area are lowered as well.

- The Loss of Wealth of Indebted Households Forced Them to Cut Back on Their Overall Spending. The decline in aggregate demand due to wealth loss of the indebted then becomes a problem for everyone in the economy.

In a new book, the economists Atif Mian and Amir Sufi have proposed a new way to set up mortgages, called Shared Responsibility Mortgages (SRM), to protect holders of underwater mortgages during a housing crisis.

Consider a house bought for $100,000 with a 20% down payment and a 30 year mortgage of $80,000 at 5% interest. The annual mortgage payment is $5,204 per year. Suppose the value of the house drops 30% to $70,000. With an SRM the owner’s equity drops to 20% of $70,000 or $14,000. The annual mortgage payment would also drop 30% to $3,643. It would continue to be adjusted each year until the house returns to 100% of original value at which point the payment would revert to and remain at the original amount unless the value again drops below 100% of original value.

In return for sharing in the loss caused by a drop in value, the mortgage holder would receive 5% of any capital gain realized whenever the house was sold or refinanced in the future.

Suppose that all mortgages in 2007 had been SRMs. All three of the problems outlined above would have been avoided. The financial crisis would have been much less severe!