This blog addresses America’s too biggest problems:

- Slow economic growth averaging just 2% since the end of the Great Recession in June 2009. Faster growth means more jobs and better paying jobs.

- Massive federal debt now 77% of GDP (for the $14 trillion public debt on which we pay interest) and predicted to continue getting worse without a change in policy. As interest rates go back up to normal historical levels the interest payments on this debt will increase greatly and be a huge drag on the federal budget.

As I have reported recently, college costs are growing much faster than healthcare costs which are growing faster than the cost of living in general. The excessive costs of education and healthcare are, in turn, holding back economic growth.

Regarding the student loan debt problem:

- For every increased dollar of student aid, college tuition increases 60 cents.

- Outstanding student loan debt has risen from $200 billion in 1996 to $1.3 trillion today.

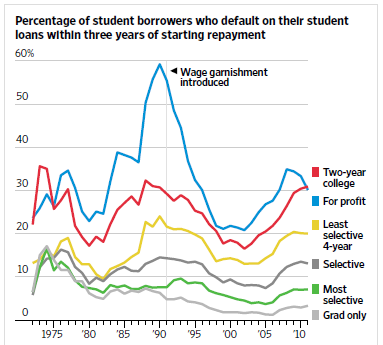

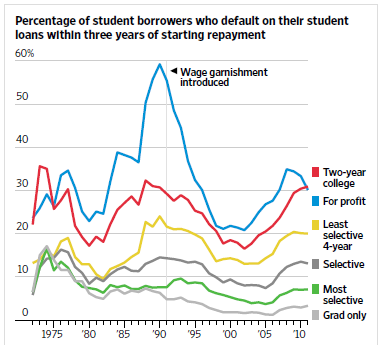

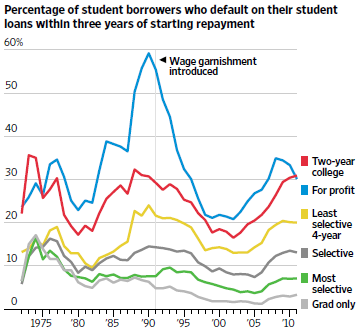

- The highest default rates on student debt occur for community college students (23%) and for-profit college students (18%).

The economist Richard Vedder has made some excellent suggestions for addressing this whole problem:

- Simplify the entire federal student air system. There should be only two programs, one grant program (Pell grants) and one federal loan program (Plus loans, tuition tax credits, work study, etc.).

- Give educational vouchers directly to students to empower recipients to weigh costs more closely. These would be strictly limited to low-income students and would be accompanied by modest academic expectations.

- Require schools to have skin in the game. Schools with abnormally high loan delinquency rates should have to pay a tuition “tax” to the government to help cover costs.

Conclusion. “Financial aid has caused tuition to skyrocket. If we can’t abolish it, we can at least simplify it.”