Student debt is a huge problem, see here and here, both for the college students and former students who have accumulated it as well as for the U.S. Government which has to carry the debt. I see this as a three-part problem which American society has to deal with:

- As illustrated in the first chart, the cost of higher education has been rising very fast in recent years, even faster than the cost of health care, which in turn is increasing faster than the underlying rate of inflation.

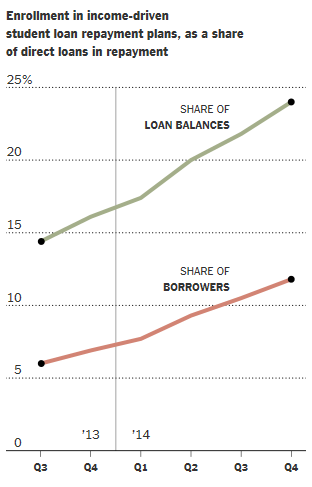

- Since 1996 outstanding student loans have risen from $200 billion to $1.3 trillion.

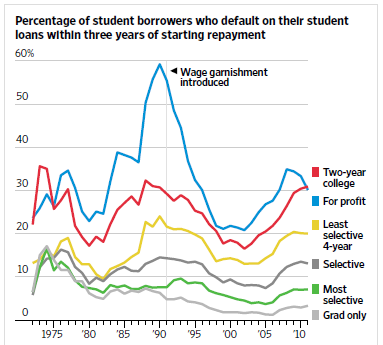

- The highest default rates on student loans occur at community colleges (23% in 2012) and for profit colleges (18%). Worst hurt are the low-income and minority students who never graduate but still have unpaid debt (see the second chart).

For the federal government to increase subsidized loan limits or to establish a broad-based free tuition program will only encourage educational institutions to keep raising their prices.

A much better approach is needed as follows:

- Faster economic growth would help immensely. Our 2% average annual growth rate since the end of the Great Recession in 2009 is simply too slow to create more jobs and higher paying jobs (which makes it easier for students to pay back their debt).

- At the federal level the emphasis should be on putting more money into Pell grants for the neediest students, paid for by cutting back on non-need based aid.

- At the state level the emphasis should be on making the two-year associate degree free for all students who pursue it. Tennessee started such a program, Tennessee Promise, in 2014, Oregon in 2016. The goal here is for many more students who try postsecondary education to end up with a degree or certificate of some sort.

Conclusion. There are positive and efficient steps which can be taken to alleviate the student debt problem for the hardest hit low-income students without aggravating the overall problem of rapidly increasing college costs.

Follow me on Twitter

Follow me on Facebook