My last post, “The Major Challenges Facing the United States,” came to the conclusion that, while the U.S. has many big problems to address, our national debt is the biggest problem of all, because it will be so hard to deal with through the political process.

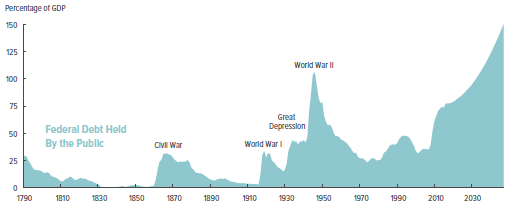

Our total national debt is now $19.9 trillion. The so-called public debt, on which we pay interest, is $15 trillion, or 77% of GDP, the highest it has been since right after WWII. Furthermore it is predicted by the Congressional Budget Office to keep getting steadily worse, reaching 90% of GDP by 2025 and 150% of GDP by 2047 unless current policy is substantially changed.

Right now our debt is almost “free” money since interest rates are so low. But when interest rates return to more normal levels, interest payments on the debt will skyrocket by hundreds of billions of dollars per year, likely leading to a new fiscal crisis, much worse than the Financial Crisis of 2008.

The only sane solution to this humongous problem is to start shrinking our annual deficits, this year at about $685 billion, down close to zero over a period of several years. This will require a painful combination of spending curtailments and perhaps some tax increases as well.

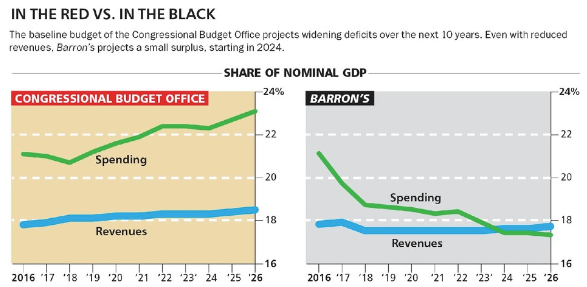

One possible way to accomplish this herculean task has been laid out by Barron’s economic journalist Gene Epstein, see here and here. Mr. Epstein’s plan would balance the budget in ten years by decreasing projected spending by $8.6 trillion, with 60% of spending curtailments coming from the entitlement programs of Social Security, Medicare and Medicaid and the rest from both military and domestic discretionary programs.

It needs to be strongly emphasized that under the Epstein plan spending would not actually decrease from one year to the next, but would rather grow at a slower rate, from $3.9 trillion in 2016 to $4.7 trillion in 2026. His plan would decrease the public debt from 77% of GDP today to 58% in 2026.

Conclusion. The U.S. faces the very unpleasant problem of excessive debt which will just keep getting worse and worse without making some relatively unpleasant adjustments in the way that the federal government spends money. The sooner we get started in this process the better off we will be.