My last several posts have expressed dissatisfaction with both presidential candidates and the hope that whoever wins in November (very likely Hillary Clinton) will work with the Republican House of Representatives to implement its “A Better Way” plan for national renewal.

In particular, faster economic growth would produce more jobs and better paying jobs and hence is highly desirable. As many people, including myself, have pointed out, it is low productivity growth caused by low business investment, which is largely responsible for slow economic growth.

The economist John Taylor has an excellent analysis of this problem. He points out that the rate of economic growth equals the growth of labor productivity plus the growth of employment.

He then shows that:

- Productivity growth slowed from the mid-1960s until the early 1980s, then increased until the mid-2000s, and has slowed way down in the past ten years.

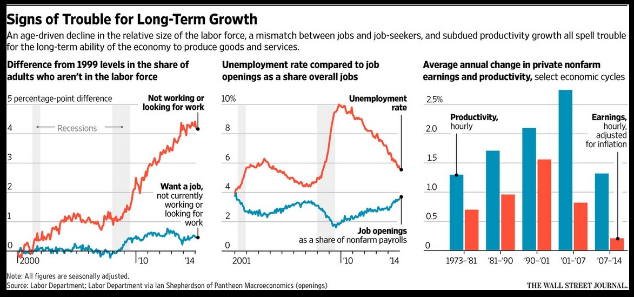

- The labor force participation rate has dropped dramatically since the Great Recession but only a small part of this drop off was caused by demographic trends (i.e. more retirees).

Such relatively long cycles of productivity growth and decline (longer than normal business cycles) suggests that government policy is having a major effect on economic performance. According to Mr. Taylor, what is needed is:

Such relatively long cycles of productivity growth and decline (longer than normal business cycles) suggests that government policy is having a major effect on economic performance. According to Mr. Taylor, what is needed is: - Tax reform to lower tax rates to improve incentives for work and investment.

- Regulatory reform to prevent regulations which fail cost-benefit tests.

- Free trade agreements to open markets.

- Entitlement reforms to prevent a debt explosion.

- Monetary reform to restore predictability in financial markets.

Conclusion. Mr. Taylor makes a very strong case that faster economic growth is not only possible but even achievable in the short run if our national leaders would just make some common sense policy changes.

Follow me on Twitter

Follow me on Facebook