As the 2016 presidential election contest begins to heat up, the Committee for a Responsible Federal Budget and its outreach arm, Fix the Debt, have issued a new “Fiscal FactChecker: 16 Budget Myths to Watch Out For in the 2016 Campaign.” Here are four of the major myths:

- We Can Continue Borrowing Without Consequences. “Low interest rates are a temporary consequence of the struggling global economy and near term Federal Reserve actions – not a permanent fixture.”

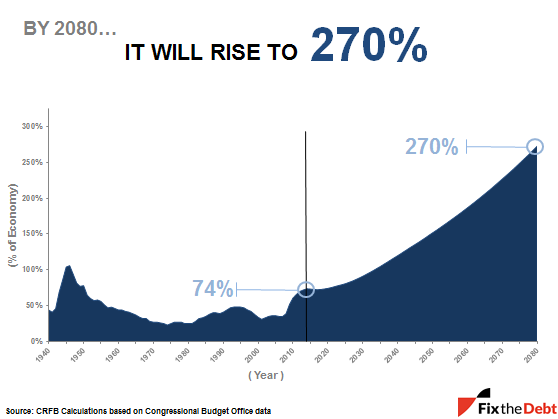

- There is No Harm in Waiting to Solve Our Debt Problems. “The longer policy makers wait to control debt, the more difficult it will become. For example, reducing debt to around the historical average of about 40% of GDP by 2040 would require tax increases or spending cuts of about 2.6% of GDP per year, if enacted today, or starting at $1,450 per person per year. Waiting a decade to begin would require adjustments of over 4% of GDP.”

- Deficit Reduction is Code for Austerity, Which Will Harm the Economy. “Most advocates of fiscal responsibility in the U.S. have called for gradual reductions in long-term deficits so that the debt grows slower than the economy. These changes tend to have minimal near-term effects as well as the potential to significantly grow the size of the economy over the long term.”

- We Can Fix the Debt Solely by Taxing the Top 1%. “The top 1% of earners, households that make at least $450,000 annually, earn a substantial share of national income, about 13% on an after tax basis, and further tax increases on this group could help. But these increases would need to be combined with reductions in spending growth and/or broader tax increases to fully address the nation’s fiscal challenges.”

Just a few days ago, I described a persuasive argument, “America’s Fourth Revolution,” that our hyper-partisan and dysfunctional political system will be unable to rectify our debt problem until we have another and much more severe financial crisis. The above discussion of budget myths from CRFB actually suggests a way forward to solve our debt problem.

We have a choice. Which path will we take?