The Federal Reserve Bank plays an important role in our economy by trying to keep inflation low and stable but also by trying to make recessions less severe by increasing the money supply when the unemployment rate is high. My last post, “What the Federal Reserve Can and Can’t Do” emphasizes that, as Ben Bernanke says, “the Fed has little or no control over long term fundamentals,” such as economic growth which depends on increases in productivity which, in turn, are heavily influenced by fiscal and regulatory policy.

The American Enterprise Institute’s Peter Wallison explains very clearly in “The slow economic recovery explained,” why, for example, the Dodd-Frank Act of 2010 is having a harmful effect on economic growth:

The American Enterprise Institute’s Peter Wallison explains very clearly in “The slow economic recovery explained,” why, for example, the Dodd-Frank Act of 2010 is having a harmful effect on economic growth:

- Regulatory burdens imposed by Dodd-Frank have been particularly harsh for community banks, with $10 billion or less in assets; 98.5 % of U.S. banks fall into this category. Since Dodd-Frank was enacted in 2010, community banks’ share of banking assets has shrunk by 12%.

- According to the Small Business Administration, there were approximately 23 million small businesses (with fewer than 500 employees) in 2012, compared to 18,500 firms with more than 500 employees. Large businesses have access to capital markets whereas small businesses rely on local banks for their credit needs.

- Regulatory costs affect small banks more than large banks because the costs are fixed, independent of size of the institution. When the Consumer Financial Protection Bureau sends out voluminous regulations on mortgage lending, for example, then extensive legal fees, compliance officers and technology retooling must be paid for up front.

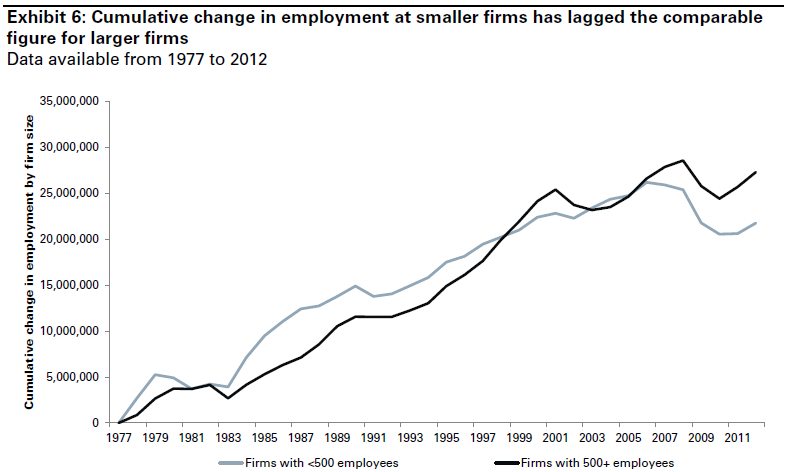

- A recent report from Goldman Sachs, “The Two-Speed Economy,” shows that large firms have grown faster than usual after 2010 while small firms have grown much slower than usual (see chart above).

Conclusion. Monetary policy alone, as conducted by the Federal Reserve, cannot return our economy to good health. This can only be accomplished by increasing productivity which is aided by smart fiscal and regulatory policy. Dodd-Frank is an example of regulatory policy which is hurting economic growth by having a harmful effect on main street banks.