The economy has been chugging along at about 2% annual GDP growth ever since the end of the Great Recession in June 2009. Unemployment has been steadily dropping and is now a fairly low 4.4%. Low wage earners are now even beginning to see bigger gains in pay.

Most people would like to speed up economic growth even more. Tax reform will help in this regard but so will sensible deregulation. Barron’s has an excellent article this week about deregulating Wall Street by William D. Cohan.

According to Mr. Cohan:

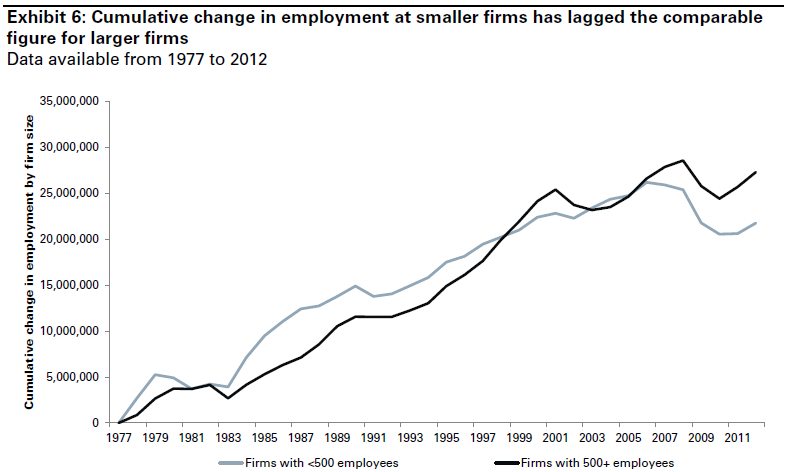

- GDP growth is highly correlated with bank lending.

- The Dodd-Frank Act, passed by Congress in 2010, has disproportionately burdened community banks, despite their having no role in the financial crisis.

- More than 1700 U.S. banks have disappeared since Dodd-Frank was passed.

- Senator John Kennedy (R, LA) has introduced a bill which would exempt community banks and credit unions with assets of less than $10 billion from the Dodd-Frank Act.

- As a result of Dodd-Frank, big banks are now required to have more capital and less leverage. Today a bank’s assets would have to fall about 7% before a bank’s capital would be wiped out, as opposed to only 2% in 2008. This makes them safer.

- Prior to 1970 the Wall Street partnership structure ensured that bankers had plenty of skin in the game – essentially their full net worth was on the line every day.

- Today bankers and traders are rewarded for taking risks with other people’s money. Mr. Cohan recommends that the top 500 traders and executives at every big bank have a significant portion of their net worth on the line.

Conclusion. Mr. Cohan’s program would not only give a big boost to the economy by enabling community banks to lend more freely but would also make our financial system safer by requiring top financiers to have skin in the game.

Follow me on Twitter

Follow me on Facebook