From a reader of my campaign website:

I am a young voter, that was not of age during the presidential election, so I am doing my research to make sure I help make a wise voting decision for our state. I understand that your main focus is the debt, and I have read up on your other issues as well, but I wanted to ask you what makes you stand out from the other candidates. I have concluded that democratic candidate Ms. Jane Raybould and you have very similar stances on issues. So, I guess my question would be what can you do for our state that other candidates haven’t brought up. I am looking forward to hearing back from you.

Here is my answer to a young, open-minded, first-time voter:

I am an unconventional candidate because I am a fiscal conservative and a social moderate, specifically:

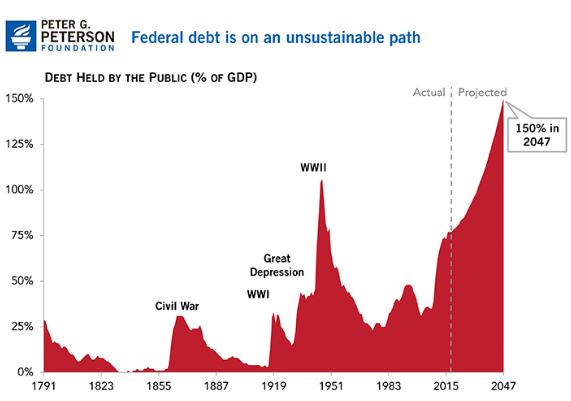

- The national debt, now 78% of GDP (for the public part on which we pay interest), is the highest since right after WWII, and is predicted by the Congressional Budget Office to keep getting steadily worse without major changes in current policy such as curtailing the growth of entitlement spending. This is by far the greatest long term problem facing our country. If we don’t address it, we will inevitably have a new and very severe fiscal crisis in the near future, as soon as interest rates return to normal (and higher) historical levels. Basically, we are in a deep hole, nonchalantly digging it deeper and deeper, when we need to devote all of our efforts to climbing out.

- Social issues such as abortion policy, gun rights and immigration reform are highly contentious but do not fundamentally threaten our prosperous and stable way of life. I am confident that the political process will eventually achieve an acceptable resolution of these social issues. I am far less confident that normal politics will get us out of our debt bind.

Conclusion. What distinguishes me from all of the other candidates in this race, Democratic, Libertarian or Republican, is my strong insistence that we must focus on solving our out-of-control debt problem. Otherwise the future of our country is at great risk. Millennials will suffer most from inaction.