You keep saying that we need lower tax rates to boost the economy but what makes you think this will help? Businesses are sitting on piles of cash. They have plenty of money to invest in expansion. What they need are more customers. The basic problem is not enough demand for more goods. This is what is holding back the economy. It doesn’t much matter what the tax rates are. If the demand and customers are there, businesses will spend their own money or borrow as much money as they need, at low interest rates, to produce all the products they can sell. Anonymous Critic

I have several responses to this criticism:

- First of all I want to make it clear that all cuts in tax rates must be offset by shrinking or eliminating tax preferences. So there will be no loss of tax revenue. Two thirds of all taxpayers take the standard deduction and will therefore automatically benefit from lower tax rates. This will put tens of billions of new dollars into the hands of middle class wage earners who will spend most of this money because they have tight budgets. This will give the economy a big boost.

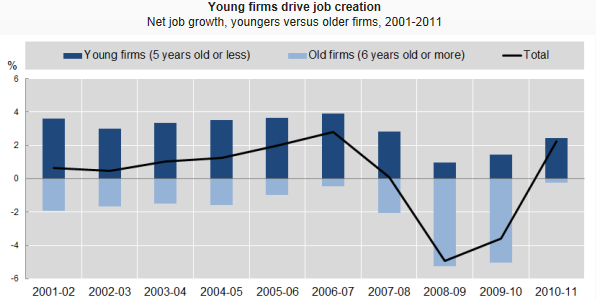

- As I discussed in my blog post from October 26, 2013 “Where are the Jobs? II. How to Create More of Them,” most net new job creation comes from businesses less than one year old, the true “startups.” New business owners are typically not wealthy, with lots of personal tax deductions. They need all the financial resources they can muster. Lower tax rates will save them money and therefore help them get their new business going.

- In general, tax deductions such as for mortgage interest, municipal bond interest payments, state and local taxes, etc. benefit the wealthiest tax payers. Therefore the lowering of tax rates, offset by shrinking tax deductions, represents a shift of funds from the wealthier to the less wealthy. This will at least slow down the increase of inequality which afflicts the modern world.

Conclusion: Lower tax rates will put more money in the hands of people who will spend it, thereby boosting the economy by creating more demand, provide support for entrepreneurs starting new businesses (which will create more jobs) and lessen income inequality. All in all this represents major progress!