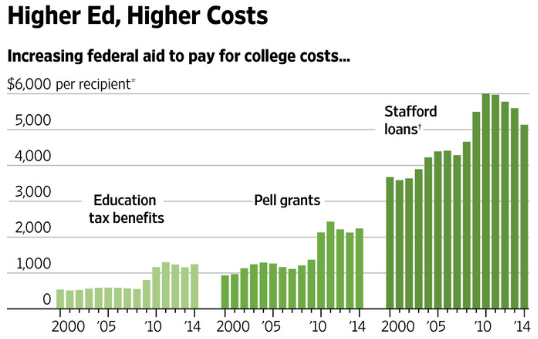

I have devoted several posts recently, here, here, and here, to discussing the rapidly increasing costs of higher education (see chart below) and the corresponding rapid rise of student debt.

Here are the basic facts:

Here are the basic facts:

- There are too few college graduates in the U.S. At least ten OECD countries have a higher percentage of college graduates than we do.

- America is graduating inequality. College degree attainment has increased between 1970 and 2011 for all income groups; however this is happening much more quickly for higher income groups.

- Not all college degrees are created equal. Students at private, nonprofit institutions graduate at higher rates, and with lower debt, than students from public institutions who, in turn, graduate at higher rates and with lower debt, than students from for-profit institutions.

- The Federal Reserve Bank of New York has found a close connection between subsidized loan and Pell Grant limits and the increase in college tuition costs.

- The Federal Reserve Bank of St. Louis has found that “white and Asian college grads do much better than their counterparts without degrees, while college-grad Hispanics and blacks do much worse proportionately.”

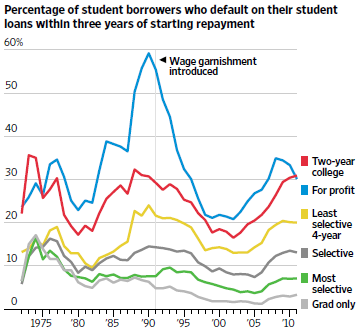

- The percentage of student borrowers at for-profit as well as community colleges who default on their loans has greatly increased since the year 2000 (see below)

In other words, our current federal student loan program is not only driving up college costs for everyone but is also creating a huge financial burden for the very low-income students who are most in need of financial aid to succeed in college.

In other words, our current federal student loan program is not only driving up college costs for everyone but is also creating a huge financial burden for the very low-income students who are most in need of financial aid to succeed in college.

The way to respond to this is to put strict lids on the amount of subsidized loans available to both undergraduate and graduate students ($30,000 and $60,000 respectively) and, at the same time, use the savings achieved in doing this to increase the size of Pell Grants available for the lowest income students who need the most help.

Conclusion: our high-tech society needs more college trained workers and we should especially encourage capable low-income young people to go to college. We could also do a much better job of targeting Pell grants instead of loans to this group of students.