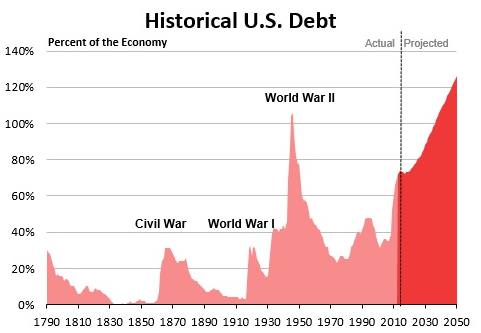

It is well understood that entitlement spending (Social Security, Medicare and Medicaid) is the biggest driver of our very serious long term debt problem. Furthermore the high costs of Medicare and Medicaid can’t be separated from the high cost of American healthcare in general. In other words, getting the cost of national health spending under control is a fundamental fiscal and economic issue.

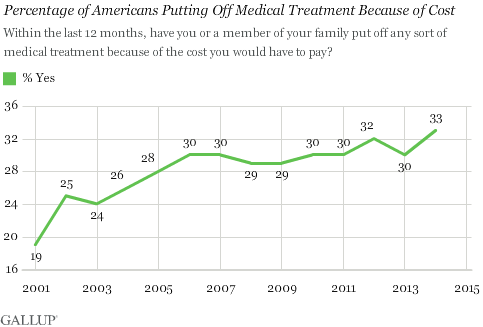

A major reason for this high cost is the tax exclusion of employer provided healthcare. American out-of-pocket spending on healthcare is only 11% of the total as compared to 26% in Switzerland or 52% in Singapore, two examples of countries with efficient free-market systems. Americans have little incentive to hold down the cost of their own care because it is mostly paid for by third party insurance companies.

A major reason for this high cost is the tax exclusion of employer provided healthcare. American out-of-pocket spending on healthcare is only 11% of the total as compared to 26% in Switzerland or 52% in Singapore, two examples of countries with efficient free-market systems. Americans have little incentive to hold down the cost of their own care because it is mostly paid for by third party insurance companies.

The Affordable Care Act (aka Obamacare) expands access to healthcare but does nothing to control overall costs. This means that any changes made to the ACA should be aimed at preserving access but making healthcare much more cost efficient. This can be accomplished by

- Keeping the Exchanges. The exchanges were set up to expand access for the uninsured and provide subsidies for those who couldn’t otherwise afford health insurance. This is the best feature of the ACA and should be retained.

- Repealing the mandates for both individuals and employers. Mandates mean that benefits have to be strictly defined, uniform for all, and therefore more expensive. Employers are burdened by extra regulations which affect hiring and growth decisions.

- Replacing the employer tax exclusion with a uniform tax credit for all. The credit would be about $2500 per person, the cost of high deductible catastrophic care. Employers could still provide insurance to employees but the tax deduction would be limited to the amount of the tax credit. The self-employed would get the same tax credit and it would also be refundable for those with low-incomes.

The American Enterprise Institute’s James Capretta describes how a transition could be made from the current ACA to such a new system.

Follow me on Twitter: https://twitter.com/jack_heidel

Follow me on Facebook: https://www.facebook.com/jack.heidel.3