My last three posts: here, here, and here, are concerned with the high cost of American healthcare and how this is so closely tied in with our very large and badly out-of-control national debt. In particular, three giant American companies: Amazon, Berkshire Hathaway, and JP Morgan Chase are forming an independent healthcare company to try to hold down healthcare costs for their combined one million employees in the U.S.

Dr. Elizabeth Rosenthal, an MD and editor-in-chief of Kaiser Health News, points out that this new company may help its own members but end up hurting the rest of us:

- Previous efforts along the same line by Safeway and Boeing have held down costs for the companies own employees but are too small scale to have had broader impact.

- The new company, much larger in size, may be able to negotiate lower prices from labs and hospitals for its own members. But then these same labs and hospitals will charge more for everyone else.

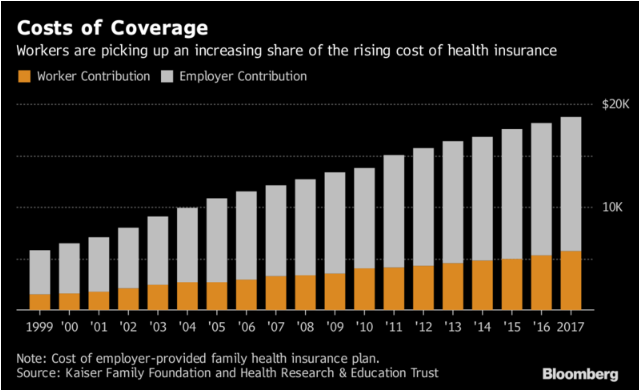

Moreover, in general, employer based healthcare insurance has lots of problems:

- It diminishes incentives to reduce costs by insulating workers from the full price of their benefits.

- It discourages changes that could displease even a small number of workers, thereby creating incentives to minimize disruption.

- The pervasiveness of employer health insurance makes it more difficult for individuals to buy health insurance on their own, thus discouraging entrepreneurship.

Conclusion. Given the inherent flaws in employer provided health insurance, it is unlikely that more innovation by individual companies, or groups of companies, will lead to an overall solution to the exorbitant cost of American healthcare.

The solution lies in a different direction: ending or at least modifying the ACA’s employer mandate. See here for details. More later!