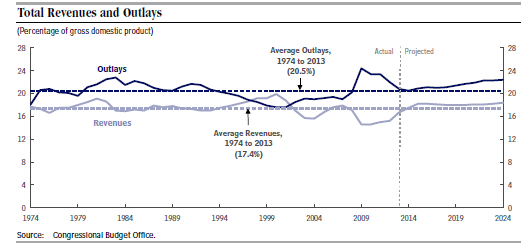

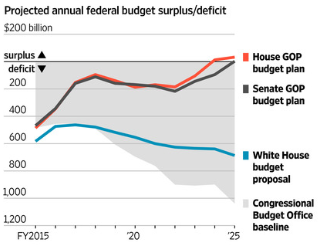

The Budget Committees for both the House of Representatives and the Senate have set a goal for balancing the federal budget over the next ten years. As can be seen in the chart below, the two committees are in remarkably close agreement as to how this ambitious goal can be reached. Once each chamber passes its own plan, then it will be up to a conference committee to produce a single unified plan.

The roughly $5 trillion in savings needed to get this done represents 10% of the approximately $50 trillion otherwise projected to be spent in the next ten years. This means that the entire federal budget, including both discretionary and mandatory (entitlements) spending, will have to be examined for savings:

The roughly $5 trillion in savings needed to get this done represents 10% of the approximately $50 trillion otherwise projected to be spent in the next ten years. This means that the entire federal budget, including both discretionary and mandatory (entitlements) spending, will have to be examined for savings:

- Preserve the Sequester spending limits but give more budget flexibility to each department. Defense hawks complain that the military budget is too tight already. But every government agency can operate more efficiently if it has to, including the Defense Department. Some very good suggestions for doing this have been given by the Heritage Foundation.

- Social Security. Simple adjustments, such as eliminating the income cap, raising the age limits for eligibility and/or moving to a more accurate index for inflation, will make the Social Security trust fund solvent indefinitely into the future. Also, eligibility for Social Security Disability Income should be tightened to allow it to operate more efficiently.

- Medicaid. The current arrangement whereby state spending is matched by the federal government, at a set percentage, is costly to both. Turning Medicaid into a block-grant program would control federal costs and give the states a big incentive to be more efficient.

- Medicare. This is the toughest nut to crack. An attractive alternative, proposed by Avik Roy of the Manhattan Institute, is to migrate Medicare over time onto the Insurance Exchanges created by Obamacare, thereby providing seniors with the same level of subsidy as everyone else.

With both the House and Senate giving high priority to setting up a ten year balanced budget plan, it is critical to seize this opportunity to address an unusually difficult problem. The future security and prosperity of our country depends on it!