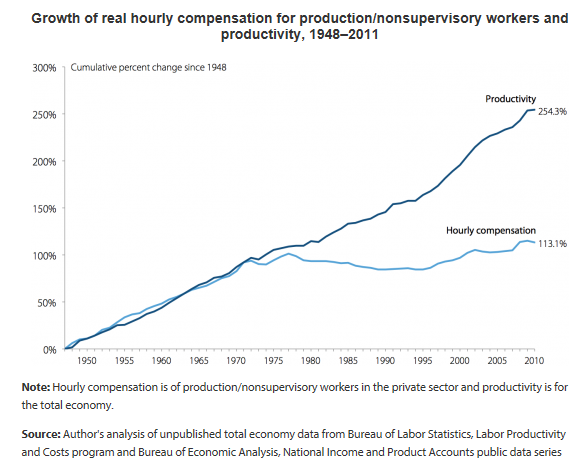

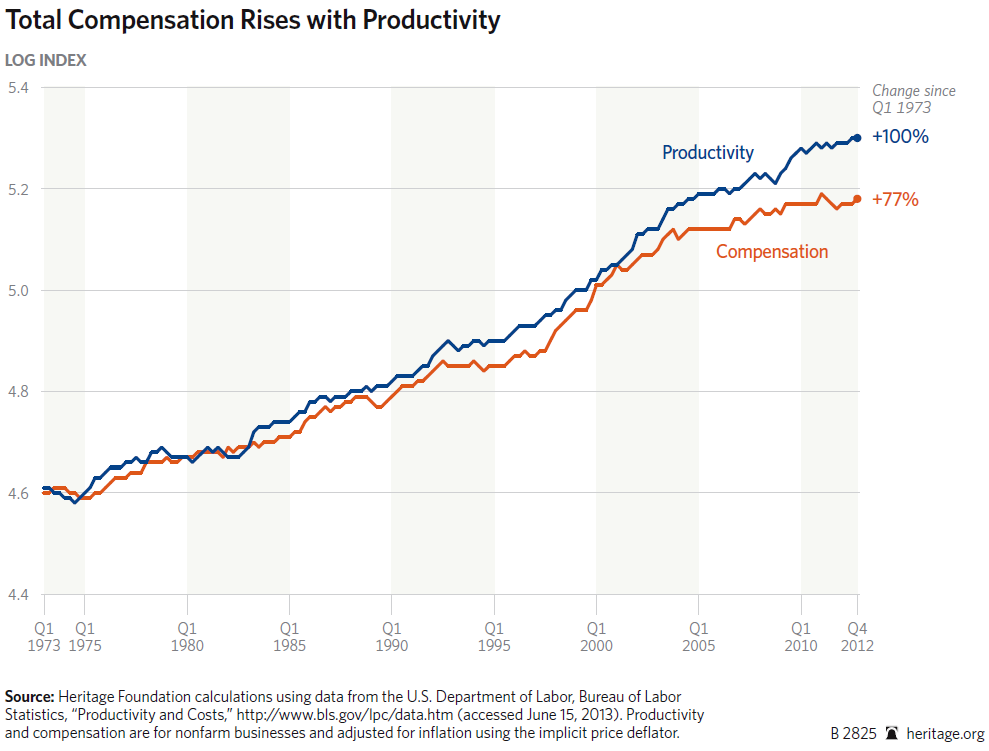

As I reported in my last blog post a few days ago, wealth inequality in the United States and the rest of the developed world is growing rapidly and is likely to get much worse in the foreseeable future. This is happening because income from wealth, i.e. the return on investment, typically grows faster than wages and GDP. As income inequality also grows, and top wage earners have more and more money to invest, then the gap between investment income and wage income will become even wider. There is nothing wrong with this and the more money that is reinvested in our economy, the faster it will grow and the more jobs that will be created.

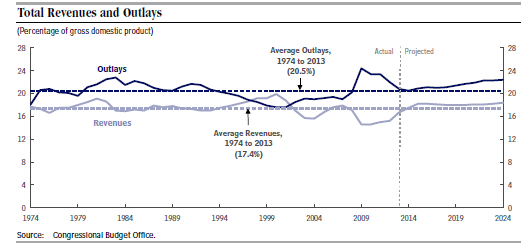

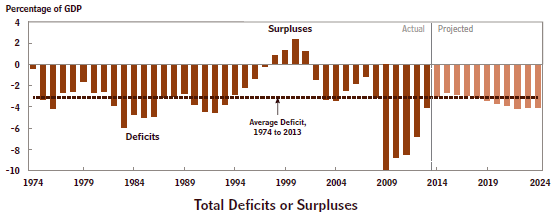

At the same time that huge new wealth is being created we have an archaic tax system in the U.S. which is not only incredibly complicated and inefficient, but also discourages investment because the top individual and corporate rates are so high. And it doesn’t collect enough tax to pay our bills. We have huge deficits already and the CBO says that they’ll just keep getting worse.

Making government operate more efficiently with less spending is highly desirable but will only go so far. Every government program has a constituency of supporters who complain when their own program is targeted for cuts. And the biggest and most expensive, the entitlement programs of Social Security and Medicare, have the largest constituency of all, over 50 million retirees at the present time and growing rapidly as the baby boomers retire at the rate of 10,000 per day.

This huge crunch can only be resolved by fundamental tax reform. Several different ways have been proposed to do this:

- Reform the current income tax system by broadening the base, lowering rates and eliminating deductions and loopholes to pay for it. The problem with this approach is that no one wants to give up their own deductions (for mortgage interest, charitable contributions, employer provided healthcare, state and municipal taxes, etc.)

- Introduce a consumption tax such as the Graetz Plan which I described in my January 7, 2014 post. It would establish a 14% Value Added Tax on consumption, supplemented by a lower but still progressive tax on incomes over $100,000. It would avoid being regressive on low wage workers by using an Earned Income Tax Credit to offset the Payroll Tax.

- Introduce a wealth tax.

Sorry, I’m over my (self-imposed) word limit already. I’ll describe a possible wealth tax in my next post!