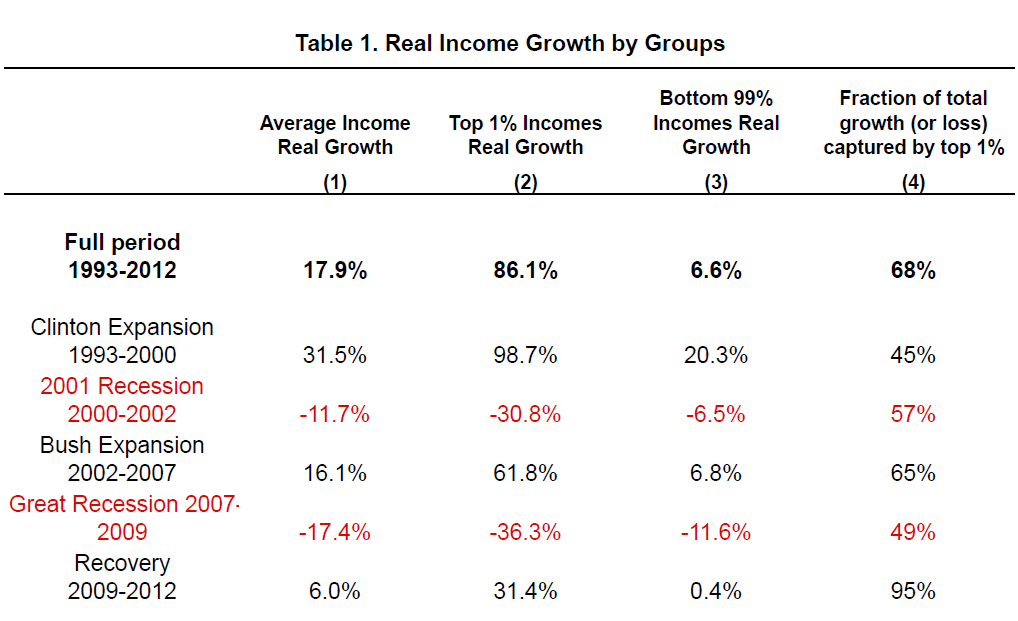

The economist Joseph Stiglitz has an Op Ed column in today’s New York Times, “In No One We Trust”, blaming the financial crisis on the banking industry. “In the years leading up to the crisis our traditional bankers changed drastically, aggressively branching out into other activities, including those historically associated with investment banking. Trust went out the window. … When 1 percent of the population takes home more than 22 percent of the country’s income – and 95 percent of the increase in income in the post-crisis recovery – some pretty basic things are at stake. … Reasonable people can look at this absurd distribution and be pretty certain that the game is rigged. … I suspect that there is only one way to really get trust back. We need to pass strong regulations, embodying norms of good behavior, and appoint bold regulators to enforce them.”  Mr. Stiglitz is partially correct. Although the housing bubble, caused by poor government policy – loose money, subprime mortgages, and lax regulation – was the primary cause of the financial crisis, nevertheless, poorly regulated banking practices made the crisis much worse. But this is all being fixed with Dodd-Frank, a just recently implemented Volker Rule, and a soon coming wind-down of Fannie Mae and Freddie Mac.

Mr. Stiglitz is partially correct. Although the housing bubble, caused by poor government policy – loose money, subprime mortgages, and lax regulation – was the primary cause of the financial crisis, nevertheless, poorly regulated banking practices made the crisis much worse. But this is all being fixed with Dodd-Frank, a just recently implemented Volker Rule, and a soon coming wind-down of Fannie Mae and Freddie Mac.

Mr. Stiglitz concludes, “Without trust, there can be no harmony, nor can there be a strong economy. Inequality is degrading our trust. For our own sake, and for the sake of future generations, it is time to start rebuilding it.

But how do we reduce the inequality in order to restore the trust which is necessary for a strong economy? Mr. Stiglitz doesn’t say!

What we need is faster economic growth in order to create more new jobs. The last four years have demonstrated that the Federal Reserve can’t accomplish this with quantitative easing. It needs to be done by private business and entrepreneurship. Tax reform and the easing of regulations on new businesses is what we need. It’s too bad that ideological blinders prevent so many people from understanding this basic truth!